Introduction

Accidents are one of the leading causes of death for younger adults, and they rarely arrive with warning. Accidental death insurance, more formally known as accidental death and dismemberment (AD&D) insurance, exists to close that specific gap. This article explains how AD&D coverage operates, how it varies from conventional life insurance, who often gains the most, and what to look for in the fine print before making a purchase.

Accidents are a leading cause of death for younger adults and often strike without warning, making accidental death and dismemberment (AD&D) insurance a critical tool for closing potential financial gaps. This article explains how AD&D coverage works, how it differs from standard life insurance, who stands to gain the most, and highlights the crucial information you need to confirm inside the fine print before making a purchase.

What Is Accidental Death Insurance? (Understanding AD&D)

Accidental death insurance is a specialized policy that pays a benefit only when death results directly from a covered accident, such as a car crash or a fall. It is not a substitute for comprehensive life insurance, which covers death from illness, old age, or natural causes as well.

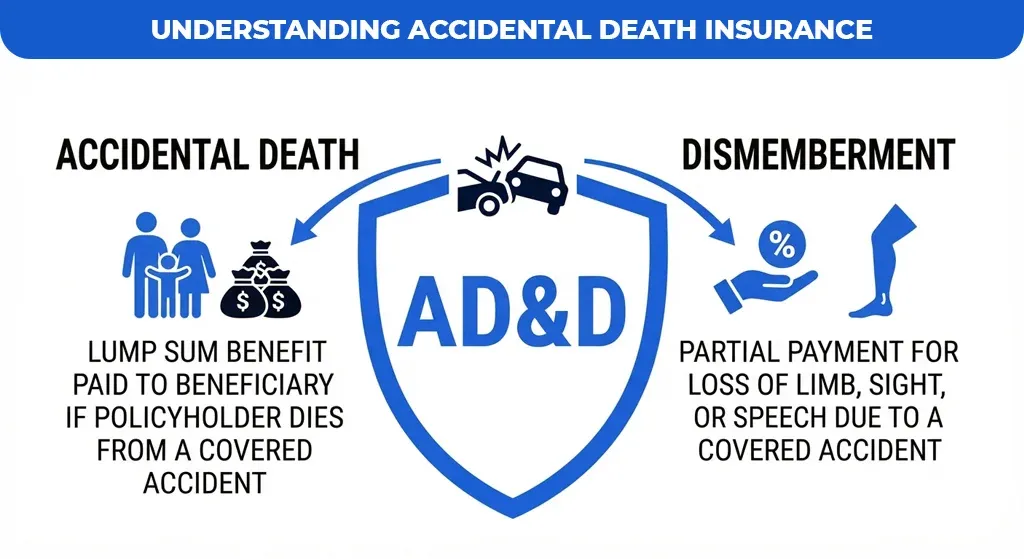

Definition: When a covered accident directly causes the policyholder’s death, AD&D insurance pays out. Common triggers include motor vehicle collisions, workplace falls, and other sudden, unexpected events.

Dismemberment component: The “D” in AD&D covers more than death. It also provides a benefit for the loss of a limb, sight, hearing, or speech resulting from a covered accident, even if the policyholder survives.

How payouts work: Death benefits are usually paid as a lump sum to the named beneficiary. Non-fatal injuries, such as the loss of a hand or an eye, typically trigger a partial payout calculated as a percentage of the full benefit.

Key distinction: In my professional experience, this is the single most misunderstood point about accidental death insurance: it is a supplemental product, not a replacement for term or whole life coverage. Clients who rely on AD&D alone can be left exposed if a death results from illness rather than an accident.

Accidental Death vs. Term Life Insurance: What’s the Difference?

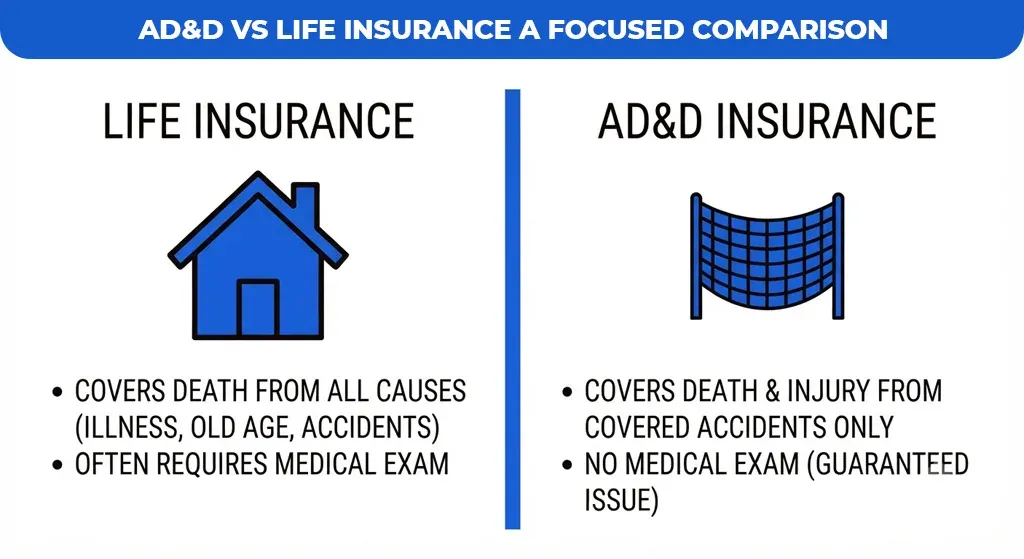

Life insurance and accidental death insurance both pay a beneficiary after the policyholder dies, but the similarities end there. The two products are complementary rather than identical since life insurance covers death from nearly any cause, whereas AD&D only pays out when an accident is the direct cause of death.

Scope of Coverage

- Life insurance: Covers death from illness, old age, accidents, and most other causes, subject to policy exclusions.

- AD&D insurance: Strictly limited to death or injury directly caused by a covered accident.

The Approval Process

Traditional life insurance often requires a medical exam or a detailed health questionnaire, and pricing is tied to health history, age, and lifestyle factors. Accidental death and dismemberment insurance is frequently “guaranteed issue,” meaning it is approved without medical underwriting, which is why it is often easier and faster to obtain.

Cost Factor

Because AD&D insurance covers a narrower set of circumstances, premiums are typically lower than comparable life insurance coverage. This makes it an attractive, low-cost addition for households looking to shore up a specific gap in protection without a large budget increase.

Quick-Reference Comparison

| Feature | Life Insurance | AD&D Insurance | Takeaway |

| Scope of Coverage | Death from nearly any cause | Death from a covered accident only | AD&D is narrower, targeted protection |

| Medical Exam | Often required | Typically not required | AD&D is faster to obtain |

| Premiums | Higher, based on health/age | Lower, flat-rate common | AD&D is budget-friendly |

| Primary Goal | Comprehensive financial support | Supplemental, accident-specific protection | Best used together, not as a substitute |

Who Should Consider Accidental Death Insurance?

Accidental death coverage tends to deliver the most value for people whose daily routines carry elevated accident risk, or who cannot easily qualify for traditional life insurance. I usually identify four groups where AD&D makes the most sense when assisting customers in assessing their coverage.

- High-risk occupations, such as construction workers, truck drivers, and law enforcement officers, face above-average exposure to workplace accidents.

- High-travel individuals, frequent flyers, and long-distance commuters spend more hours in transit, where accident risk accumulates.

- AD&D’s guaranteed-issue coverage is still available to conventional life insurance applicants who are rejected due to pre-existing conditions and are not eligible for traditional underwriting.

- Budget-conscious families and households that want an affordable safety net layered on top of, or in place of, more expensive coverage while they build a fuller financial plan.

Understanding the Fine Print: Exclusions and Limitations

Insurance companies specify precisely which circumstances do not fall under the purview of covered accidents, and AD&D policies are strictly defined by design. Reading these exclusions before purchasing a policy is the best way to avoid an unpleasant surprise at claim time.

Common Exclusions

- Death from natural causes, illness, or disease.

- Suicide or other self-inflicted injury.

- Death occurring during an illegal act or while under the influence of drugs or alcohol.

- Injuries sustained during hazardous hobbies, such as skydiving or mountain climbing, unless a rider is added.

Insurers, not policyholders, define what counts as “accidental,” and that definition can be tested in court when an underlying medical condition contributed to the accident. It’s worth asking an agent directly how a specific insurer handles borderline cases before you rely on a policy for coverage.

Conclusion

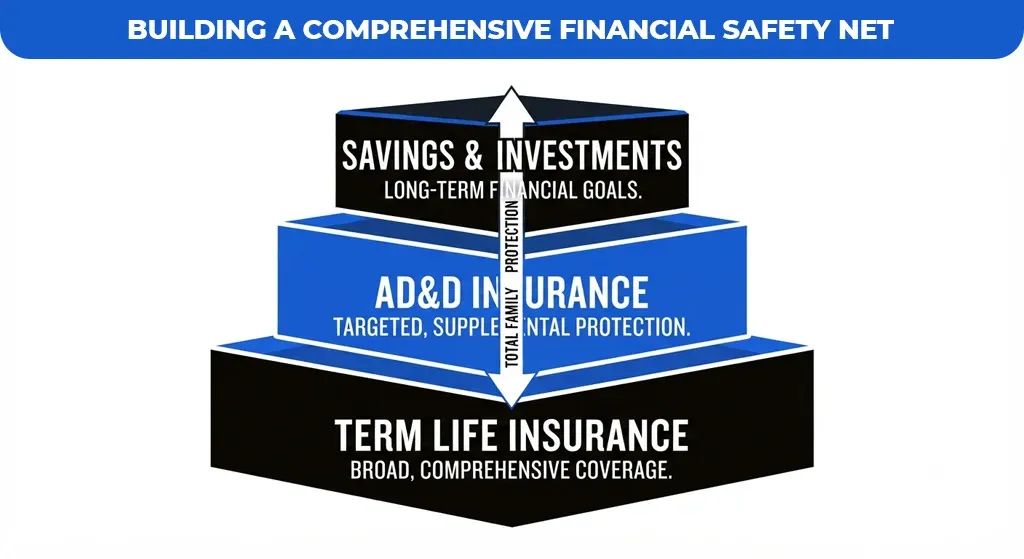

Accidental death insurance serves as an essential, high-value component of a robust financial strategy, specifically designed to provide an immediate and affordable safety net for families facing the unexpected volatility of life. While it is crucial to recognize that this coverage is not a comprehensive replacement for traditional life insurance, its role as a strategic, supplemental tool is unmatched, particularly for those in high-risk occupations, frequent travelers, or individuals navigating the complexities of pre-existing conditions that might otherwise hinder access to standard underwriting.

Take control of your financial destiny by auditing your current employer-provided benefits and existing policies to identify where these vital safety nets might be missing. Do not leave your family’s long-term security to chance; instead, reach out to an experienced professional today to determine if a tailored accidental death insurance policy is the missing piece in your comprehensive financial safety net.