Introduction

Every parent or homeowner shares a common, quiet worry: “What happens to my family if I’m no longer here?” It’s a heavy question, but protecting your family’s financial future doesn’t require a massive sacrifice from your monthly budget. There’s a persistent myth that real protection is expensive. It isn’t.

Many people skip buying coverage entirely because they assume it’s out of reach, leaving their loved ones financially exposed. Affordable term life insurance is the most straightforward way to close that gap: a large safety net for a fraction of the cost of a permanent policy.

This guide breaks down exactly how affordable term life insurance works, exposes a pricing trap hiding inside many workplace plans, and gives you a step-by-step method for locking in the lowest affordable term life insurance rate you qualify for.

What Is Term Life Insurance, and Why Is It So Affordable?

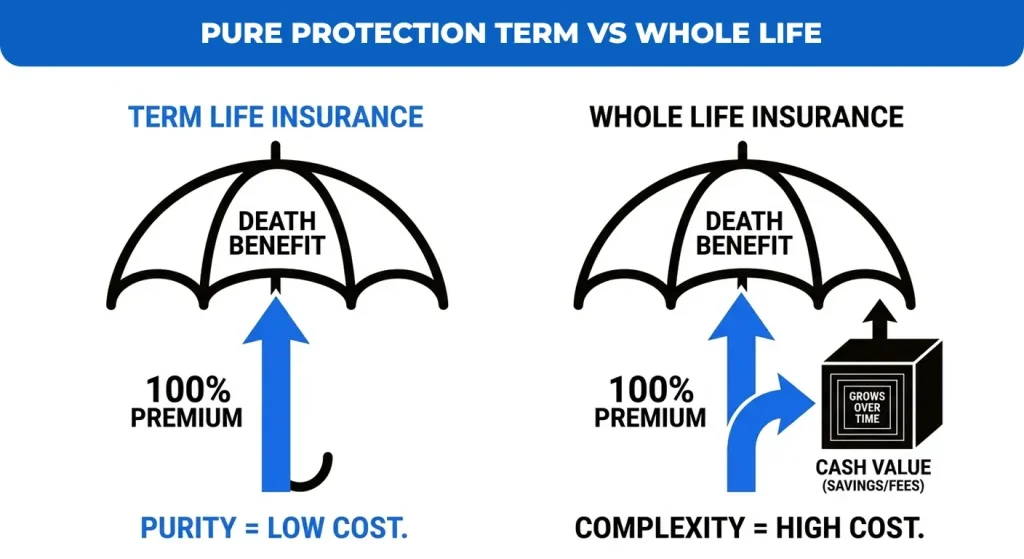

Term life insurance is coverage that lasts for a fixed period, typically 10, 15, 20, or 30 years. Your beneficiaries will get a tax-free death benefit if you pass away within that time frame. If you outlive the term, the policy simply ends (unless you renew or convert it).

The reason an affordable term life insurance policy costs so little compared to permanent insurance comes down to what you’re actually buying. Term is pure protection; there’s no investment or cash-value account attached, so none of your premium is being diverted into savings, fees, or commissions, the way it is with whole or universal life.

Because the insurer is only on the hook for a defined window rather than your entire lifetime, and because most buyers are younger and healthier when they apply, the underwriting risk is lower, and that risk is what sets the price. Industry research from LIMRA (Life Insurance Marketing and Research Association) has consistently found that level term premiums for a healthy applicant can run at a small fraction of the cost of permanent coverage with an identical death benefit.

Term vs. Whole Life at a Glance

| Feature | Term Life Insurance | Whole Life Insurance |

| Coverage length | Fixed period (10–30 years) | Lifetime |

| Monthly cost | Low pure protection | High includes cash value |

| Cash value | None | Builds over time |

| Best for | Replacing income, covering debt/mortgage | Estate planning, lifelong needs |

Individual Level Term vs. Group “Level Benefit” (The Naming Trap)

Not every policy marketed as “level” actually keeps your costs level. This is where shopping for the best affordable term life insurance plan gets confusing, because two products can look identical on the surface and behave completely differently over time.

Individual level term: For the duration of the policy, both your premium and your death benefit are fixed. You pay the same amount in year one as you do in year twenty.

Group “level benefit” plans: Many employer-sponsored group policies keep the payout level but quietly increase your premium every five years as you age. A rate that looks cheap at 30 can become a serious expense by 50, often without much warning.

Industry trap to watch for: A group policy advertised as “level” usually refers to the death benefit, not the premium. Read the rate schedule before assuming your workplace coverage is locked in; the premium column is where the real cost is hiding.

Hypothetical 15-Year Cost Comparison

The numbers below are illustrative, not a quote, but they show the pattern insurers see again and again: an escalating group premium overtakes a locked individual rate well before the policy term ends.

| Policy Type | Monthly Premium, Year 1 | Monthly Premium, Year 15 | 15-Year Total (approx.) |

| Individual-level term | $28 | $28 (unchanged) | $5,040 |

| Group “level benefit” term | $18 | $95 (age-banded increases) | $9,700+ |

How to Choose Your Term Length Based on Life Milestones

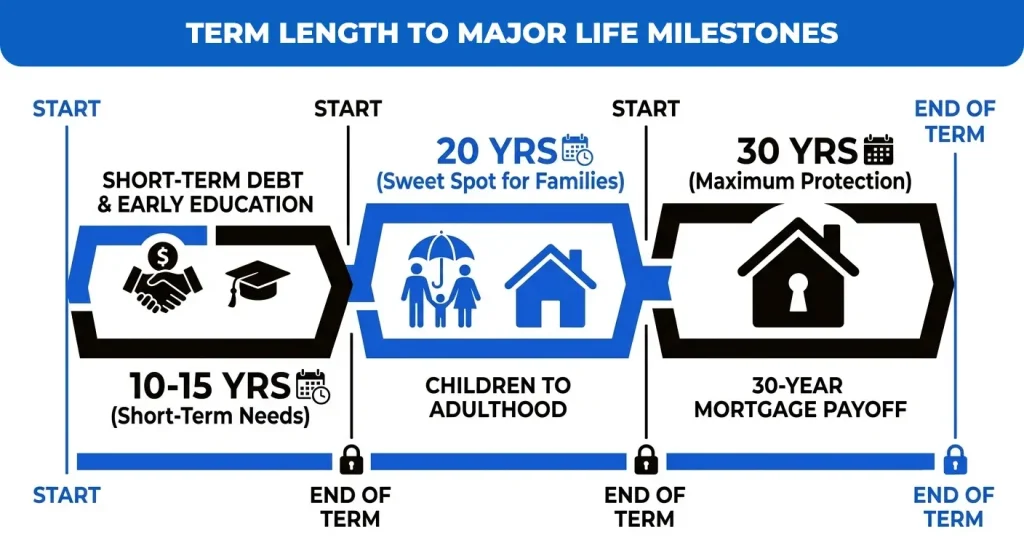

Choosing the best term length is largely a matter of matching your years of coverage to the lifespan of your largest financial obligations, ensuring you do not pay for protection you no longer need. For those with short-to-medium-term liabilities, a 15-year term is often the ideal choice for older parents wanting to shield their children through college graduation, or for individuals looking to cover a specific personal loan. If you need a bit more runway, a 20-year term serves as the ultimate “sweet spot” for young families, offering a reliable safety net that protects newborns all the way until they reach adulthood and financial independence.

For long-term financial security, a 30-year term offers the maximum duration typically available and is best paired with major milestones like buying a home. By matching a 30-year policy with a brand-new 30-year mortgage, you guarantee that the family home stays entirely paid off if the unexpected happens. Whether you are protecting a growing family or securing a lifelong investment, picking the right timeline ensures your budget is never strained by unnecessary premiums.

Steps to Lock In the Cheapest Affordable Term Life Insurance Rate

Once you know your term length, these five levers do the most to bring your affordable term life insurance quote down.

- Buy as young as possible. Premiums typically climb roughly 8–10% for every year you wait, so the cost of delay compounds quickly.

- Optimize your health classification. Quitting smoking, managing blood pressure, or losing even modest weight before you apply can cut your premium significantly. Insurers reward measurable health improvements.

- Calculate your actual coverage gap. Add your mortgage balance, other debt, and years of income replacement your family would need, rather than guessing a round number that’s larger (and pricier) than necessary.

- Pay annually instead of monthly. Most carriers knock 2–5% off the total premium when you pay once a year instead of in monthly installments.

- Compare affordable term life insurance quotes online. Independent brokers let you run multiple carriers side by side in minutes, which is the single fastest way to find the most affordable term life insurance rate you personally qualify for.

Affordable Term Life Insurance for Every Life Stage

Cost isn’t the only variable that changes from person to person, age, health history, and even employment background, which makes affordable term life insurance plans make sense.

Affordable Term Life Insurance Over 50 and for Seniors Over 60

Term coverage doesn’t disappear once you turn 50. Many insurers still offer affordable term life insurance for seniors, typically in 10- or 15-year terms, aimed at covering a remaining mortgage balance or a spouse’s income gap rather than lifelong needs.

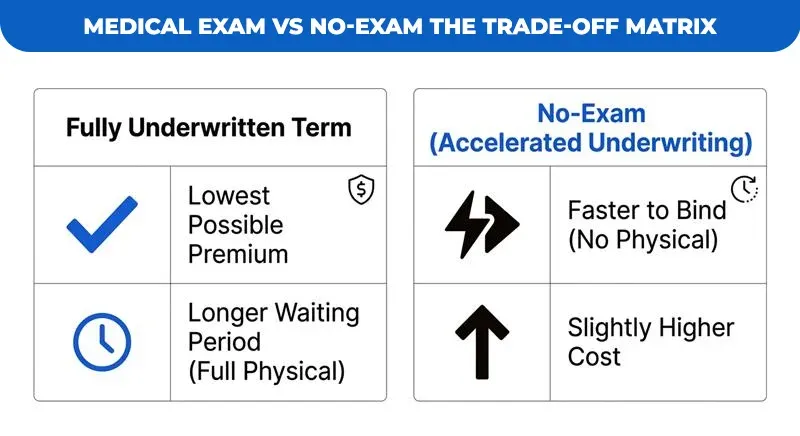

Affordable Term Life Insurance No Medical Exam

No-exam (accelerated underwriting) term policies use health records, prescription history, and a questionnaire instead of a physical. They’re faster to bind but usually cost somewhat more than a fully underwritten term, a reasonable trade-off if you need coverage in place quickly.

Affordable Term Life Insurance for Veterans and Smokers

Veterans can often supplement or replace SGLI/VGLI coverage with a private, affordable term life insurance policy that stays level for a full 20 or 30 years rather than needing periodic renewal. Smokers will pay a higher rate class than non-smokers, but shopping multiple carriers matters even more here, since insurers vary widely in how strictly they define “tobacco use.”

Conclusion

Securing affordable term life insurance isn’t about cutting corners on your family’s safety—it is a calculated, high-leverage strategy to shield your life milestones without wasting a single dollar on bloated, unnecessary policy features. Locking in an individual-level term policy while you hold the advantage of youth and health remains the absolute most powerful lever you control to permanently freeze rock-bottom rates. Delaying this decision only compounds your financial risk, while taking action today builds an ironclad safety net around your loved ones.

Stop leaving your family’s financial survival to chance. Seize complete control of your future right now by claiming free, budget-friendly term life insurance quotes from at least three premier independent carriers this week. Instantly compare the rates, robust term lengths, and underwriting classes side by side to dominate your financial planning before prices climb a single dollar higher.

Ready to see your own numbers?

Stop leaving your family’s financial survival to chance. Visit Assurance Gurus today to claim your free, budget-friendly term life insurance quotes from top-tier independent carriers. Instantly compare rates, custom term lengths, and underwriting classes side-by-side to lock in your peace of mind before prices climb.