Planning for the cost of your own funeral is not a comfortable exercise. Most people put it off for years, and many never get around to it at all. But the alternative, leaving grieving family members to scramble for cash while also arranging a service, often does more damage than the conversation ever could. In my experience working with clients in their 60s and 70s, the single biggest regret I hear isn’t “I wish I’d bought coverage sooner.” It’s “I wish my kids hadn’t had to pay for this out of pocket.”

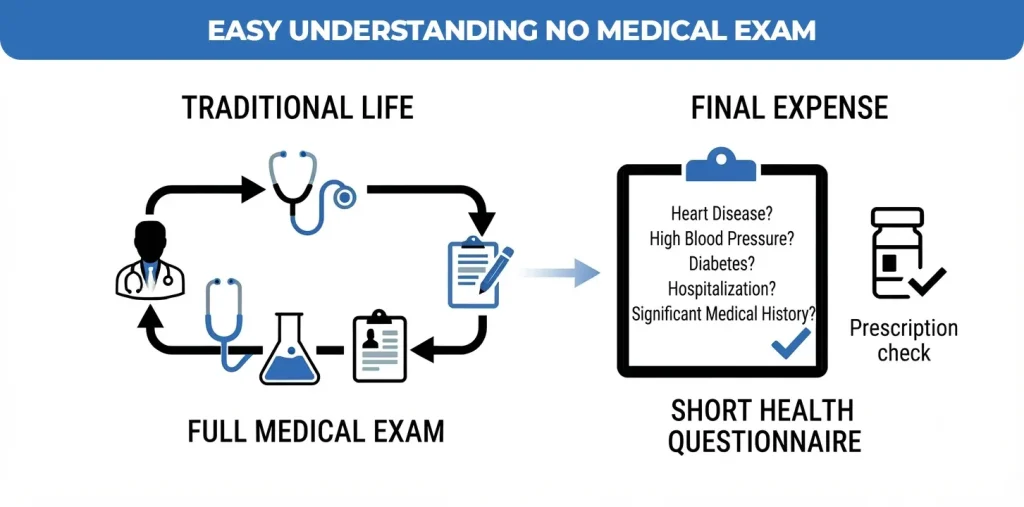

Final expense life insurance (also called burial insurance or funeral insurance) is a small, permanent whole life policy built specifically to cover the costs that show up in the days immediately following a death. Unlike traditional life insurance, it’s designed to be easy to qualify for; many policies require no medical exam at all, and it exists purely to eliminate one specific source of financial stress at the worst possible time.

This guide walks through what final expense life insurance actually covers, how it differs from term and traditional whole life insurance, the four main policy structures carriers offer, how to calculate the coverage amount you actually need, and what to check before you sign anything.

What Is Final Expense Life Insurance?

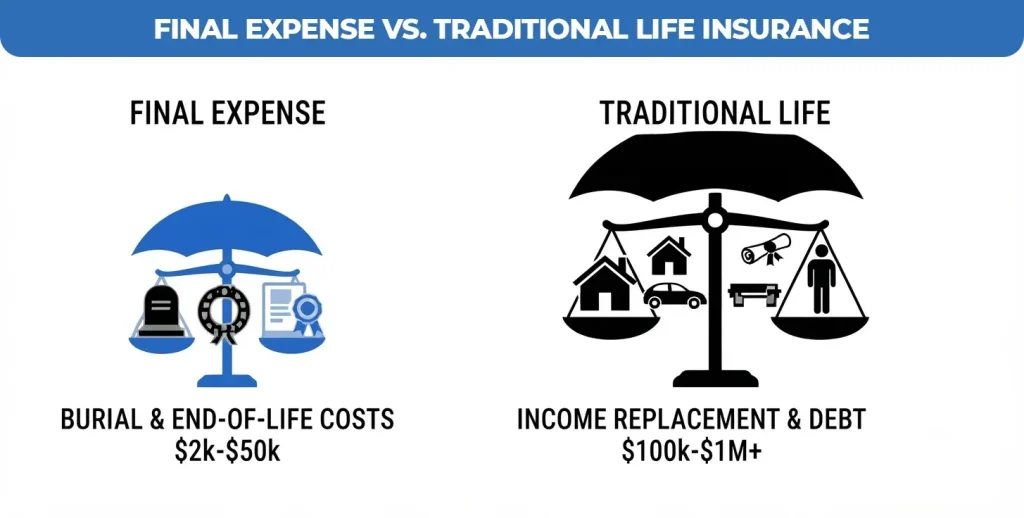

Final expense life insurance is a permanent whole life policy with a modest death benefit, typically $2,000 to $50,000, that pays a tax-free lump sum to your named beneficiary to cover costs associated with your death. It’s underwritten differently than standard life insurance: most carriers use a short list of health questions instead of a medical exam, which speeds up approval and opens the door to applicants who might not qualify for larger policies.

The name describes the intended purpose, but the payout itself is not restricted. Once the death benefit is paid, your beneficiary can use it however they see fit. In practice, most families put it toward:

- Funeral home services, burial, or cremation costs

- Caskets, urns, and burial plots

- Outstanding medical bills or hospice care

- Remaining small debts or final utility bills

Why does this matter now more than ever? The National Funeral Directors Association’s most recent General Price List Study puts the median cost of a funeral with viewing and burial at $8,300, and a funeral with cremation and services at $6,280, and neither figure includes the cemetery plot, headstone, or vault, which can add several thousand dollars more. For comparison, Social Security’s death benefit has been frozen at $255 since 1954. That gap is precisely what final expense coverage is built to close.

Final Expense vs. Traditional Life Insurance

Final expense insurance is a form of whole life insurance, but it’s built around a narrower use case than a standard term or whole life policy. The core distinction comes down to purpose: final expense exists to cover a fixed, relatively predictable cost, while term and traditional whole life are built to replace income or build long-term wealth for beneficiaries.

| Feature | Final Expense | Term / Traditional Whole Life |

| Coverage Amount | $2,000–$50,000 (most policies land between $5,000–$25,000) | $100,000–$1,000,000+ |

| Medical Requirements | Typically, there is no test, a shortened health assessment, or a guaranteed problem | Full medical exam typically required, especially above $250,000 |

| Policy Duration | Permanent lasts for life as long as premiums are paid | Term: expires after 10–30 years. Whole life: permanent |

| Primary Goal | Cover funeral, burial, and end-of-life costs | Replace lost income, pay off a mortgage, fund dependents’ futures |

| Underwriting Speed | Days, sometimes same-day approval | Weeks, pending exam and records review |

When to Choose Which

Final expense life insurance tends to fit seniors, or anyone with a health condition that would make traditional underwriting difficult or expensive. If your goal is narrowly to make sure your funeral and immediate final bills don’t fall on your family, this is the more efficient product, as you’re not paying for underwriting complexity or coverage size you don’t need. Term life insurance remains the better fit for someone still working, with dependents, a mortgage, or income that needs replacing if they die unexpectedly.

Understanding the Four Main Types of Policies

Final expense carriers generally sell coverage through one of four underwriting structures. The difference between them comes down to how much health information the insurer collects and how quickly your full death benefit becomes active.

- Level Benefit: Full coverage is active from day one, provided you’re approved. This is typically reserved for applicants in reasonably good health who pass a simplified health questionnaire.

- Graded Benefit: Coverage steps up gradually over the first two to three years. If death occurs from natural causes during that window, beneficiaries receive a reduced payout rather than the full face amount; accidental death is usually covered in full immediately.

- Modified Benefit: Similar to graded, but the payout during the initial waiting period, often the first two to three years, is typically limited to a return of premiums paid, plus interest, rather than any portion of the face value.

- Guaranteed Issue: No medical questions at all, approval is essentially automatic within the eligible age range (usually 50–85). The trade-off is a mandatory waiting period, commonly 24 months, before the full death benefit activates for non-accidental death.

In my experience, guaranteed issue final expense life insurance gets oversold to applicants who would actually qualify for cheaper, faster-paying simplified issue coverage. If you can answer a short health questionnaire honestly and pass it, level benefit coverage is almost always the better value.

How to Determine Your Coverage Needs

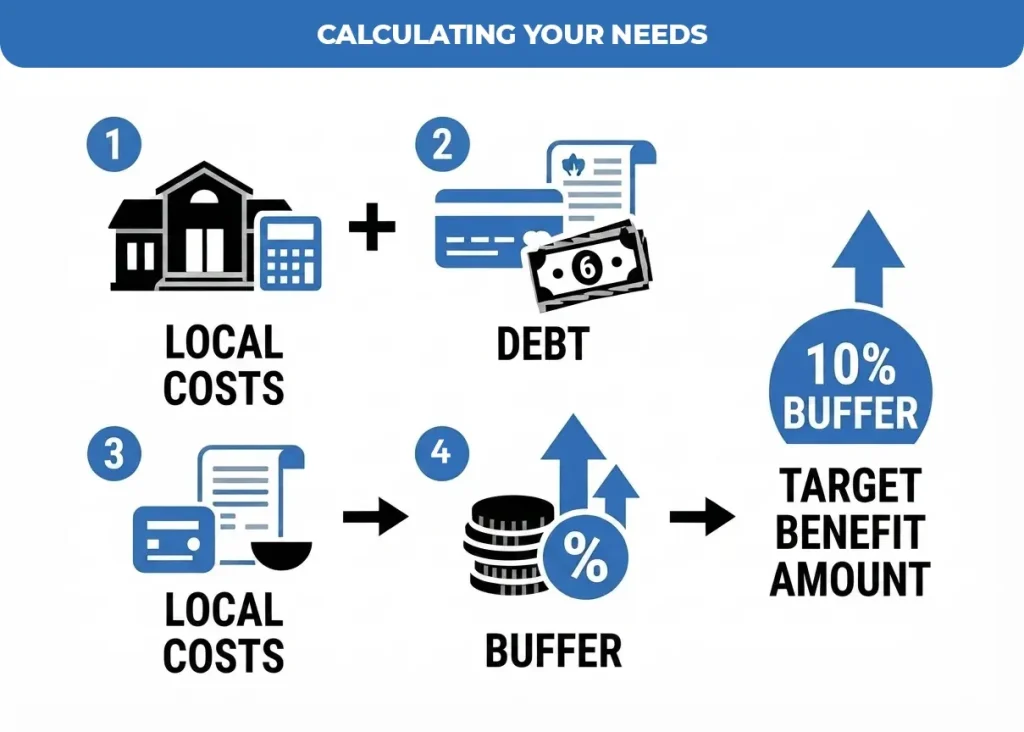

The right death benefit for a final expense whole life insurance policy is the number that covers your local funeral costs, any debt you don’t want passed on, and a reasonable buffer, no more, no less. Overbuying just raises your premium without adding real protection.

A simple three-step calculation:

- Research local funeral costs for both burial and cremation. Funeral home pricing varies by region. NFDA data shows Northeast costs running as much as 30%+ above the national median, while Southern states often run below it. Ask a local funeral home for its General Price List; the FTC’s Funeral Rule requires them to provide one on request.

- Add outstanding medical or credit card debt you’d want the policy to help clear, since these obligations don’t disappear at death and can fall to the estate or, in some cases, a surviving spouse.

- Build in a buffer, typically 10–15% for inflation and unforeseen add-ons like cemetery fees, a headstone, or transportation costs, which usually aren’t included in published funeral averages.

If you’d like a more precise number based on your location, age, and existing coverage, a life insurance calculator or a licensed agent can run the math against current local pricing rather than a national average.

Conclusion

Securing a final expense life insurance policy is one of the most meaningful steps you can take to protect your family from the sudden financial and emotional burden of end-of-life costs. By shifting the responsibility away from your loved ones, you ensure that your final wishes are honored without the stress of unexpected bills, allowing your family to focus on what truly matters during a time of grief.

Now is the ideal time to evaluate your specific needs, compare personalized quotes, and lock in affordable, permanent protection that fits your budget. Reach out to a licensed professional today to review your options and secure the peace of mind that comes with knowing your legacy is protected and your final expenses are fully covered.

Have a specific health condition or budget concern?

Not every applicant is the same, and neither is every policy. If you have questions about your specific health history or need help calculating an exact benefit amount for your area, the team at Assurance Guru is here to help. We make the process simple, transparent, and fast.