Introduction

Most people understand they need life insurance. Far fewer act on it, and almost nobody fully understands it. That gap is dangerous. A term life insurance plan is the financial safety net your family depends on if the unthinkable happens, yet millions of households either skip it entirely or buy the wrong type for the wrong reasons.

I have spent years helping families and business owners navigate the life insurance landscape. The single most consistent observation: the people who regret their decisions almost always chose complexity over simplicity, or delayed because they found the topic intimidating. This guide removes that barrier.

Term life insurance plans are built on a simple idea: pure protection for the years your family needs it most. Whether you have just bought your first home, started a family, launched a business, or taken on significant debt, the right term plan turns financial vulnerability into security.

How Term Life Insurance Plans Work

A term life insurance plan is a contract between you and an insurance company. You pay a fixed premium for a defined period. If you die within that term, the insurer pays a tax-free lump sum to the beneficiaries you name. If you outlive the term, the policy expires with no payout unless you added a Return of Premium rider.

That simplicity is the product’s greatest strength. There are no investment components, no hidden fees, and no ambiguity about what you are getting.

Key Terms Explained

- Death Benefit: The one-time payment made to your heirs. Also called the face amount or sum assured.

- Level Term: The most common structure. Your premium stays fixed for the entire policy duration.

- Policy Term: The duration of coverage, typically 10, 15, 20, 25, or 30 years.

- Beneficiary: The person or entity who receives the death benefit. You choose who this is.

- Underwriting: The process by which the insurer assesses your health and lifestyle to set your premium.

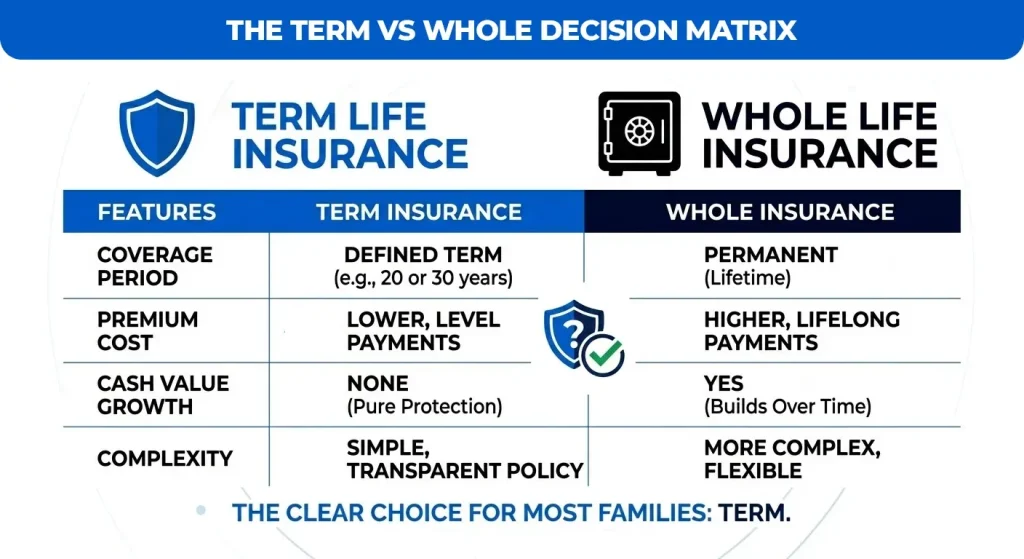

Term Life vs. Whole Life: The Core Difference

The comparison below cuts through the noise. Most families are best served by term, but the right answer depends on your financial goals.

| Feature | Term Life Insurance | Whole Life Insurance |

| Coverage Period | Fixed term (1030 yrs) | Lifetime / Permanent |

| Premiums | Low & fixed | Higher & fixed |

| Cash Value | None | Yes (grows over time) |

| Best For | Income replacement, mortgages, young families | Estate planning, lifelong dependents |

| Complexity | Simple & transparent | Complex |

Key insight: Whole life is not better; it is just different. For income replacement, mortgage protection, and education funding, term life insurance plans deliver significantly more coverage per premium dollar. Reserve whole life insurance policy where you genuinely need lifelong coverage.

Who Needs a Term Life Insurance Plan?

Term life insurance is not for everyone in every situation. But if you fall into any of the categories below, it belongs in your financial plan.

Life Stage Checklist

- You have a spouse, partner, or children who depend on your income

- You carry a mortgage or significant personal debt

- You are self-employed or run a business with partners or employees

- Your family would struggle financially if your income stopped tomorrow

- You are the primary caregiver and your household could not easily replace the services you provide

If you checked three or more, you need a term life insurance plan.

Specific Buyer Profiles

Young Professionals and New Families

This is the sweet spot for best term life insurance plans. You are young and healthy; premiums are at their lowest. Locking in a 20- or 30-year term now guarantees affordability even as you age. Coverage should reflect income replacement for the years until your children are financially independent.

Mortgage Holders

Align your term length with your loan repayment schedule. A 25-year mortgage calls for a 25-year term plan. This ensures your family keeps the home regardless of what happens to you.

Business Owners

Keyperson insurance, a term plan on a critical employee or founder, protects business continuity. It gives the company breathing room to recruit, retrain, or wind down without financial catastrophe. Buy-sell agreements funded by term plans also protect business partners.

Parents Planning for Education

Factor in projected college or university costs for each child. A 20year term started when your child is born provides coverage through the years they would need financial support most.

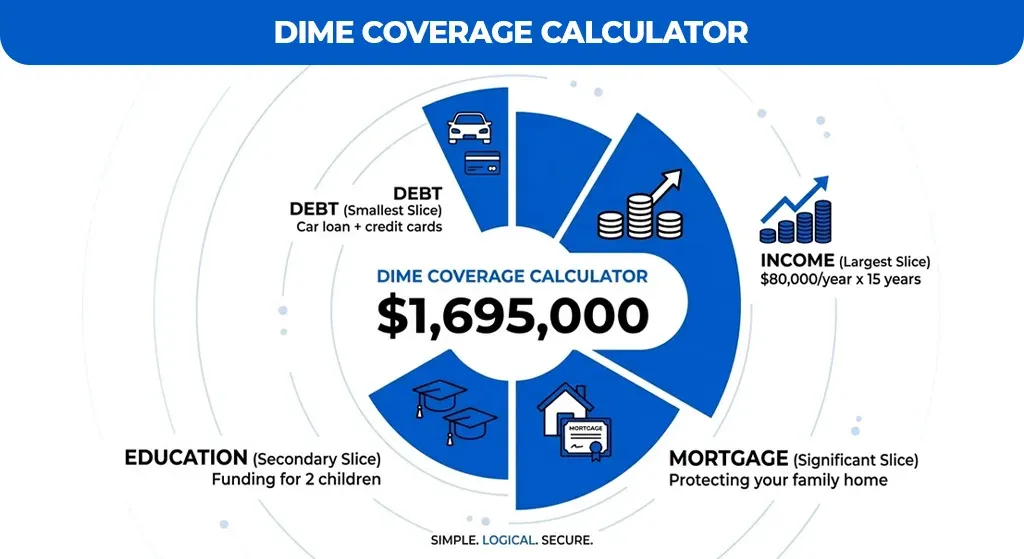

How to Calculate Your Coverage Needs: The DIME Formula

Guessing your life insurance coverage is a mistake that costs your family dearly. The DIME formula is the most reliable, practical method for calculating a needs-based coverage amount.

A Worked Example

Consider a 35yearold professional with these figures:

- Debt (excl. mortgage): $15,000 (car loan + credit cards)

- Income replacement: $80,000/year x 15 years = $1,200,000

- Mortgage balance: $280,000

- Education (2 children): $100,000 each = $200,000

Total DIME Coverage Needed: $1,695,000

In practice, rounding up to $1.7 million or $2 million makes sense. Inflation will erode purchasing power over time, and slightly overinsuring is far less costly than underinsuring.

The Inflation Factor: Do Not Ignore It

A death benefit of $1 million today will have significantly less purchasing power in 20 years. When calculating income replacement, add a 34% annual inflation buffer to future projections. Many online life insurance term plan calculators do this automatically; use them as a second check.

Customizing Your Policy: Riders and Flexibility

A standard term life insurance plan is excellent protection on its own. Riders are optional add-ons that expand that protection to cover specific scenarios.

Which Riders Are Worth It?

- Always consider: Waiver of Premium and Critical Illness. These address high-probability scenarios: disability and serious illness that many people face before death.

- Consider carefully: Return of Premium raises your premium by 3050%, but refunds 100% if you outlive the term. It makes sense only if cash flow allows and you are disciplined enough not to cancel early.

- Situational: Conversion Privilege is invaluable if your health may decline or your financial situation will change significantly.

Factors That Influence Your Premiums

Life insurance pricing is not arbitrary. Every factor below is measurable, and understanding them puts you in control of your cost.

Age

The most powerful factor. A healthy 30-year-old pays roughly 5060% less than a healthy 40-year-old for the same coverage. Every year you delay costs money.

Health History

Insurers review your medical records, current conditions, family history, and BMI. Controlled chronic conditions raise premiums but rarely disqualify applicants. Uncontrolled or complex conditions have a larger impact.

Smoking Status

Smokers pay 23x more than nonsmokers for identical coverage. Many insurers reclassify you as a nonsmoker after 12 months of cessation one of the most cost-effective steps you can take before applying.

Coverage Amount and Term Length

Longer terms and higher face amounts mean higher premiums. But there is a nuance: premium bands. Buying $1,000,000 of coverage can sometimes cost less per $1,000 than buying $750,000, because the higher face amount moves you into a better pricing tier. Always compare quotes at adjacent coverage levels.

Lifestyle and Occupation

High-risk hobbies (skydiving, rock climbing) and occupations (mining, offshore drilling) trigger underwriting surcharges. Disclose these accurately; misrepresentation is the number one cause of claim denials.

Approximate Premium Guide (NonSmoker, Healthy)

| Age / Gender | $500K / 20yr | $1M / 20yr | $1M / 30yr |

| 30 / Male | ~$22/mo | ~$38/mo | ~$58/mo |

| 30 / Female | ~$18/mo | ~$32/mo | ~$48/mo |

| 40 / Male | ~$38/mo | ~$68/mo | ~$108/mo |

| 40 / Female | ~$30/mo | ~$55/mo | ~$88/mo |

| 50 / Male | ~$95/mo | ~$175/mo | ~$290/mo |

| 50 / Female | ~$72/mo | ~$135/mo | ~$220/mo |

The Honesty Principle Critical for Claims

No section of this guide is more important than this: be completely truthful on your application. Disclose every medical condition, medication, surgery, family history item, and lifestyle detail the insurer asks about.

Misrepresentation, even unintentional, gives the insurer legal grounds to deny your beneficiaries’ claim. That denial happens at the worst possible moment. Transparency during underwriting protects your family when it matters.

Online vs. Offline Applications

Online life insurance term plans have democratised access. You can compare term life insurance plans across multiple providers, complete underwriting, and receive a policy number within days without an agent. The key advantage is transparency: you see every number, every exclusion, and every rider cost before committing.

Complex health histories, high-value policies, and business-purpose insurance still benefit from an experienced broker who can negotiate underwriting terms on your behalf.

Conclusion

Securing a term life insurance plan is the most decisive, high-impact step you can take to architect your family’s absolute financial independence. By prioritizing this essential safety net today, you replace paralyzing uncertainty with ironclad security, ensuring your loved ones are shielded from catastrophe regardless of life’s unpredictable turns.

Do not wait for a life-changing event to evaluate your coverage; the optimal time to lock in rock-bottom premiums is while you are young and healthy. Take control of your legacy now, compare personalized quotes from top-rated providers, and invest in the incomparable peace of mind that comes from knowing your future is protected, guaranteed, and fully secure.

FAQs

Is it worth having term life insurance?

Yes, it is essential for anyone with dependents or debt. Term plans offer the highest death benefit per dollar spent, providing affordable, crucial financial security to protect your family’s future effectively.

Can someone with a pacemaker get life insurance?

Yes, in most cases. Insurers evaluate your overall cardiovascular health and the underlying reason for the device. Many people with stable heart conditions qualify for coverage, often with standard or rated premiums.

How much does a $1,000,000 term life insurance policy cost?

A healthy 30-year-old non-smoker typically pays $30–$45 monthly for a 20-year term. Costs increase with age and smoking status. Always obtain multiple quotes, as pricing varies significantly between different insurance providers and carriers.

If I have cirrhosis, can I still obtain life insurance?

Early-stage, compensated cirrhosis may qualify for coverage from specialist insurers at higher premiums. Advanced stages are more difficult. Honest disclosure is vital, and working with an impaired-risk broker can significantly improve options.

What is the monthly premium for a $500,000 life insurance policy?

For a healthy 35-year-old non-smoker, expect to pay roughly $20–$45 monthly, depending on gender and age. These figures are benchmarks; your actual premium depends on your specific health classification and chosen term length.