Introduction

Whole life insurance cost is the first question most families ask, and it’s the right one. On average, a healthy 35-year-old can expect to pay $200–$400 per month for a $500,000 whole life policy. But that number alone tells only half the story. Unlike term insurance, every dollar you pay builds a growing, tax-advantaged asset that belongs to you for life. This guide breaks down every factor that drives the cost of whole life insurance, shows you exactly what you are getting in return, and gives you actionable strategies to make permanent coverage affordable at any age or budget.

Why Whole Life Insurance Costs More Than Term

When comparing permanent life insurance premiums to term, the difference can feel dramatic, sometimes 5 to 15 times higher for the same death benefit. Here is why that gap exists, and why it may be worth it.

The ‘Permanent’ Premium Explained

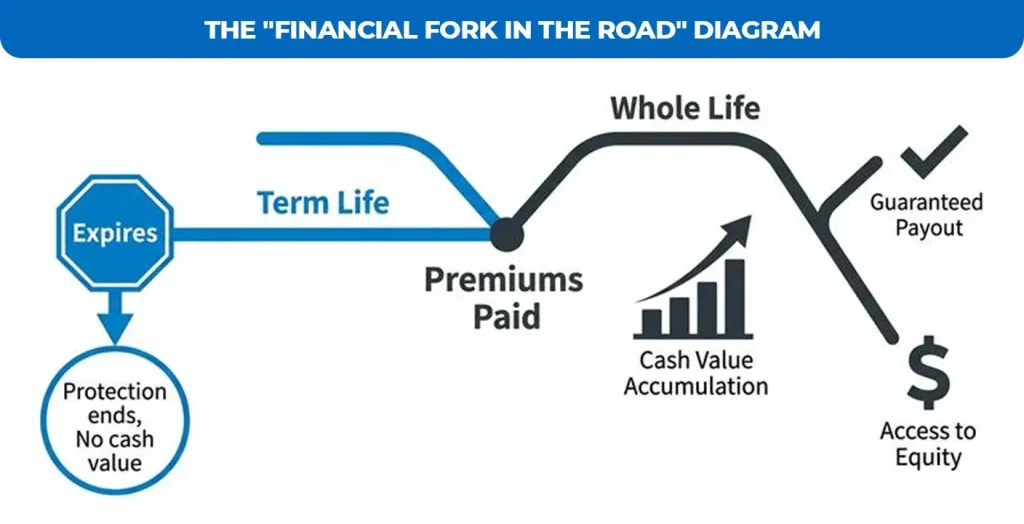

Term insurance is time-limited. You pay for coverage during a specific window, say, 20 years. If you outlive the term, the insurer keeps your premiums, and the contract ends. Whole life insurance, by contrast, is engineered to pay out guaranteed. The insurer prices this certainty into every premium. Fixed premiums never increase, even as you age or your health changes.

The Investment Component: Where Your Premium Goes

A portion of every whole life premium is allocated to a cash value account that grows on a tax-deferred basis. This is the single biggest cost driver and the most misunderstood benefit. Over a 20- or 30-year horizon, this accumulated cash value can rival or exceed the total premiums you have paid in, making the ‘cost’ of the policy a far more nuanced calculation.

Whole Life vs. Term: Side-by-Side Comparison

| Feature | Whole Life Insurance | Term Life Insurance |

| Coverage Duration | Permanent (lifetime) | Fixed period (10–30 yrs) |

| Premium Stability | Fixed never changes | Increases at renewal |

| Cash Value | Yes grows tax-deferred | No |

| Death Benefit | Guaranteed | Only if in-term death |

| Dividends | Yes (participating policies) | No |

| Average Monthly Cost* | $200–$1,000+ (age 35, $500K) | $25–$50 (age 35, $500K) |

| Best For | Lifelong coverage + wealth | Temporary income protection |

Primary Factors Influencing Your Whole Life Insurance Cost

Underwriters assess several variables when calculating your personalized premium. Understanding these factors gives you leverage before you apply.

Age at Issue: The Most Powerful Variable

Every year you delay, the cost of whole life insurance often rises by 8–12% annually. The table below illustrates the long-term financial impact of waiting. [INSERT: Cost of Waiting Timeline Infographic suggested placement here]

| Age at Issue | Monthly Premium | Annual Premium | 30-Year Total | Lifetime Savings vs. Age 45 |

| 25 | $150 | $1,800 | $54,000 | Save $54,000+ |

| 30 | $185 | $2,220 | $66,600 | Save $32,400+ |

| 35 | $240 | $2,880 | $86,400 | Save $14,400+ |

| 40 | $320 | $3,840 | $115,200 | Save $0 (baseline) |

| 45 | $450 | $5,400 | $162,000 |

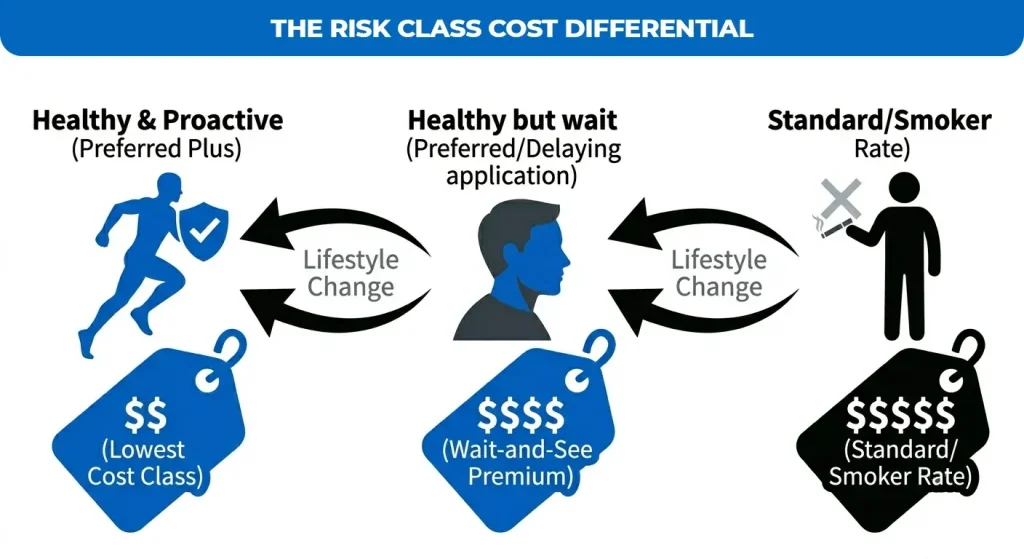

Health and Lifestyle: Your Underwriting Profile

Insurers assign applicants to risk classes, typically Preferred Plus, Preferred, Standard Plus, and Standard. A lower risk class means a lower premium. Here are the primary underwriting variables:

- Medical history (heart disease, diabetes, cancer history)

- Current height/weight ratio and BMI

- Use of tobacco (smokers pay two to four times as much as non-smokers)

- Family history of hereditary conditions

- Prescription medication history

| PRO TIPSmall lifestyle changes in the 12 months before your application can move you into a better risk class. Quitting tobacco for 12+ months, achieving a healthier BMI, and getting chronic conditions under active medical management are among the highest-impact moves. Some insurers also reward consistent lab values. |

Face Amount: Death Benefit Size

The death benefit you select has a direct, linear relationship to your monthly premium. The cost of a $100,000 whole life insurance policy will be roughly one-fifth of a $500,000 policy for the same applicant. Choosing the right coverage amount, not simply the highest available, is key to balancing protection with budget. The DIME formula in the next section helps you determine that target number.

Beyond the Premium: True Cost vs. Long-Term Value

Understanding Dividends on Participating Policies

Many whole life policies issued by mutual insurance companies are ‘participating,’ meaning policyholders share in the company’s profits through annual dividends. While dividends are not guaranteed, many leading mutual carriers have paid them consistently for over 100 consecutive years. Policyholders can use dividends to: reduce annual premiums, purchase paid-up additions (increasing both death benefit and cash value), or simply receive them as cash.

Strategies to Manage and Optimize Your Costs

Choosing the Right Payment Structure

How long you pay premiums significantly affects your annual cost. Two primary structures exist:

- Life Pay: Life Pay (Ordinary Whole Life): You pay premiums for your entire life. The monthly cost is lowest, but you are paying indefinitely. Best for those who prioritize the smallest possible monthly outlay.

- Limited Pay: Limited Pay (10-Pay or 20-Pay): You pay higher premiums for a compressed period (10 or 20 years), then the policy is fully paid up. You retain the death benefit and cash value for life without further payments. Best for those with high current income who want to eliminate future premium obligations.

Policy Riders: Add Value Carefully

Riders customize your coverage, but can inflate costs unnecessarily. Here is a balanced view:

Riders that typically add strong value:

- Waiver of Premium Rider Premiums: If you become completely disabled, your premiums are waived.

- Guaranteed Insurability Rider: purchase additional coverage without re-underwriting

- The Accelerated Death Benefit Rider provides benefits early if diagnosed as terminally ill

Riders to evaluate carefully (often add cost with limited benefit):

- Return of Premium Rider is often overpriced relative to the benefit

- Accidental Death Benefit has a statistically low claim probability; it is rarely cost-effective

The Role of Cash Value in Reducing Your Long-Term Net Cost

Calculating Net Cost: The True Measure of Value

Over a 20-year horizon, a well-designed whole life policy can result in a near-zero net cost, meaning the cash value you have accumulated roughly equals what you have paid in premiums. In some scenarios, particularly with strong dividend performance, the net cost can actually turn negative, meaning your policy has returned more value than it cost you.

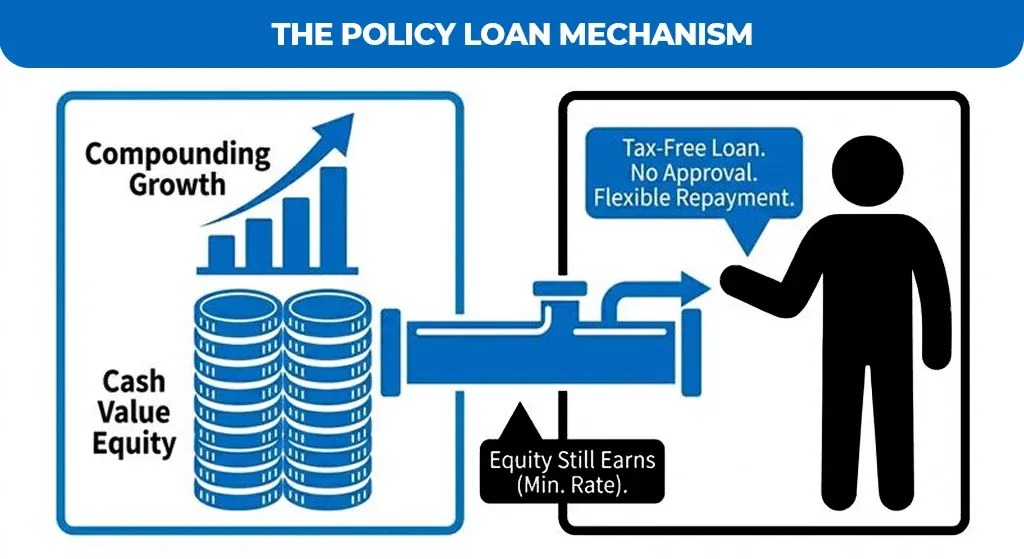

Policy Loans: Strategic Access to Liquidity

One of the most powerful and least understood features of permanent life insurance is the ability to borrow against your cash value at competitive rates, without a credit check, and without triggering a taxable event. Unlike a bank loan:

- No loan approval process or credit impact

- Flexible or no fixed repayment schedule

- Your cash value continues to earn interest or dividends even while borrowed against

- Loan proceeds are received income-tax-free

| IMPORTANT CAUTIONARY NOTEOutstanding policy loans reduce your death benefit dollar-for-dollar. If a loan is not repaid and the policy lapses, the forgiven loan balance may become taxable income. Always work with a licensed advisor to manage loan activity within your policy’s guidelines. |

Tax Advantages of Cash Value Life Insurance

The tax treatment of whole life insurance cash value is a significant long-term benefit that is rarely factored into premium cost comparisons:

- Tax-deferred growth: your cash value grows without annual income tax

- Tax-free access loans and partial withdrawals (up to basis) are generally not taxable

- Income-tax-free death benefit beneficiaries receive the full death benefit free of federal income tax

- Estate planning efficiency with a proper ownership structure, and benefits can be excluded from the taxable estate.

Conclusion

When considering the true whole life insurance cost, it is essential to reframe your perspective: this is not merely a recurring expense, but a strategic financial commitment designed to secure your family’s future while building guaranteed wealth. While permanent premiums command a higher initial investment than temporary term options, you are securing far more than a death benefit—you are acquiring a powerful, tax-advantaged asset that offers lifelong stability.

Ultimately, the most critical question is not simply “can I afford this?” but rather, “can I afford the staggering financial risk of waiting?” You lose out on years of compound growth and the instant protection of your insurability with each year of delay, which results in higher premiums.

Stop Overpaying and Start Securing Your Future.

Life insurance premiums only go up as you age. Lock in your rates today and start building tax-advantaged cash value immediately. Join thousands of families who trust Assurance Guru to navigate their permanent life insurance options. Get My Free Quote.

Frequently Asked Questions

How much does a $1,000,000 whole life insurance policy cost per month?

A $1,000,000 policy typically costs a healthy 35-year-old non-smoker between $400 and $900 monthly, depending on the insurer and risk class. At age 45, this coverage generally runs $700–$1,400 per month.

Will life insurance pay out for cirrhosis?

Yes, an existing policy usually pays the full death benefit regardless of the cause, including liver cirrhosis. However, active liver disease often affects your ability to qualify for new coverage.

How much does a $300,000 whole life insurance policy cost?

For a standard 40-year-old male, this policy typically costs $180–$350 monthly. Rates vary significantly based on your gender, health classification, and insurer, with top-tier ratings potentially reducing premiums by over 20%.

Why does Dave Ramsey advise against purchasing whole life insurance?

He argues that term insurance plus investing the savings typically outperforms whole life. This perspective suits simple protection needs but ignores the whole life’s unique benefits for complex estate or business planning.