Introduction

Financial landscapes shift, careers change, families grow, and retirement draws near. Your

Life insurance coverage should evolve alongside every one of those moments. In our experience reviewing hundreds of policies, the most common regret we hear is: “I wish I had known this was flexible.” This guide fixes that.

Below, we break down exactly how a universal life insurance policy works, explore the indexed and variable variants, compare it fairly against whole life and term, and give you a decision framework you can act on today.

How Does a Universal Life Insurance Policy Work?

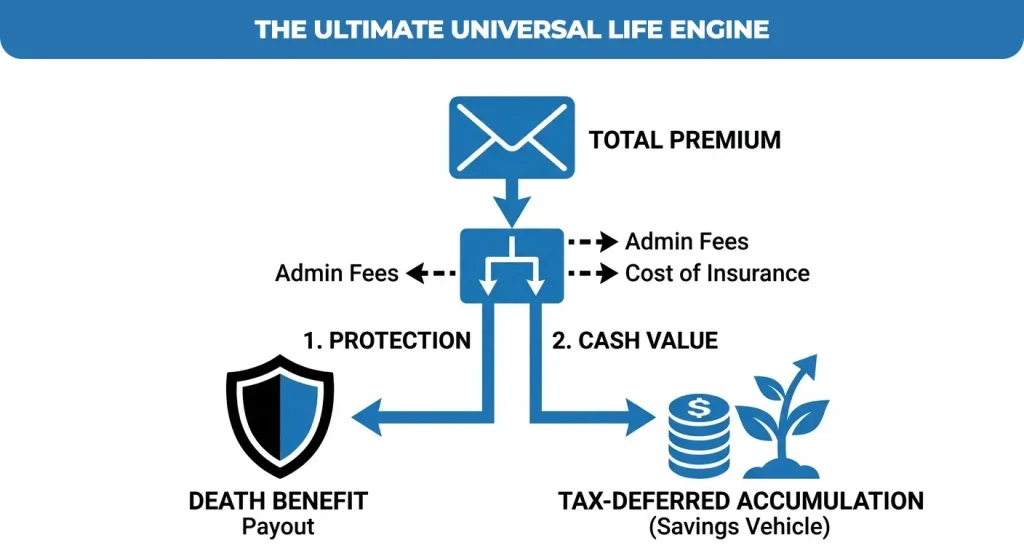

At its core, every universal life insurance policy contains two components working in parallel: a death benefit (the payout your beneficiaries receive) and a cash value account (a savings vehicle tied to the policy). Each premium you pay is split between the two.

Flexible Premiums: Pay More, Pay Less, or Pause

Unlike whole life policies, where the premium is locked in at issue, universal life gives you a target premium, a minimum premium, and a maximum premium. You can adjust your payment within that range at almost any time. If your business has a strong quarter, you can overfund the policy to accelerate cash value growth. If you face an unexpected expense, you can temporarily reduce or skip a payment, provided the cash value can cover the internal cost of insurance.

Common pitfall we see: Policyholders make minimum payments during low-interest-rate environments and are blindsided years later when the cash value has eroded, and the policy is on the verge of lapse. Active monitoring is not optional; it is a requirement of this product.

Adjustable Death Benefit: Increase or Decrease Coverage

As your financial obligations evolve, children leave home, a mortgage gets paid off, or a business interest is sold, you may need less coverage. Universal life policies typically allow you to decrease the death benefit without underwriting. Increases, however, require evidence of insurability, and some carriers will decline applicants in declining health.

Most policies offer two death benefit options: Option A (Level), which pays a flat benefit, and Option B (Increasing), which pays the face amount plus the accumulated cash value. Option B carries higher internal charges but delivers more total value to beneficiaries if cash value grows substantially.

The Role of Cash Value in Universal Life Insurance

The cash value component is what separates universal life insurance policies from term products and what creates both the greatest opportunity and the greatest complexity.

How Cash Value Grows

Traditional (Fixed) Universal Life: Cash value earns a declared interest rate set by the insurer, subject to a contractual minimum (often 2%–3%). Growth is steady and predictable but modest.

Indexed Universal Life (IUL) Insurance Policy: Without direct market exposure, credit rates are based on the performance of a market index, often the S&P 500. Policies include a floor (usually 0%) to protect against market losses and a cap or participation rate that limits upside. What is an index universal life insurance policy’s key advantage? You participate in market gains with a protective floor, a middle ground between the guarantees of whole life and the upside of variable products.

Variable Universal Life (VUL) Insurance Policy: Cash value is invested directly in sub-accounts similar to mutual funds. You bear full investment risk; values can decrease, but the upside is uncapped. VULs are securities products requiring FINRA licensing to sell.

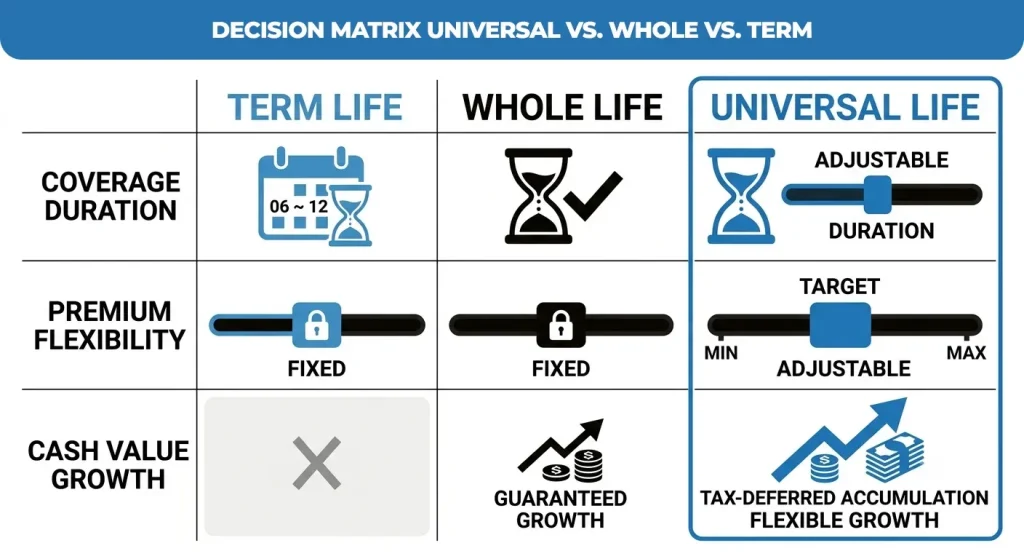

Universal vs. Whole vs. Term Life Insurance: Side-by-Side

Understanding where a universal life insurance policy fits requires an honest comparison of all three product families. Use the table below as your reference.

| Feature | Universal Life | Whole Life | Term Life |

| Coverage Duration | Lifetime | Lifetime | Fixed Period (10–30 yr) |

| Premium Flexibility | High – adjustable | Fixed | Fixed |

| Death Benefit | Adjustable | Guaranteed fixed | Fixed |

| Cash Value Growth | Interest / Index / Market | Guaranteed rate | None |

| Tax-Deferred Growth | Yes | Yes | No |

| Policy Loans | Yes | Yes | No |

| Complexity | Moderate–High | Low | Very Low |

| Best For | Flexible long-term planning | Guaranteed certainty | Affordable short-term coverage |

Our take: Whole life wins on guarantees. Term life wins on price for temporary needs. Universal life wins when you need permanent coverage with the ability to adapt over a 30–50 year horizon. The right answer depends entirely on your specific financial architecture.

Types of Universal Life Insurance Policies: Know Before You Buy

Fixed (Traditional) Universal Life

The foundational product. Predictable crediting, straightforward mechanics, lower internal volatility. Best for conservative clients who want flexibility without market-linked complexity.

Indexed Universal Life Insurance Policy (IUL)

The area of the life insurance market that is expanding the fastest. An indexed universal life insurance policy links cash value growth to a market index while protecting against loss via a floor. IUL pros and cons to know: The floor eliminates downside risk in bad market years, but caps and participation rates mean you will not capture full index returns. Spread the illustrations across multiple index crediting strategies to get a balanced picture.

Indexed universal life insurance policy reviews from policyholders often cite pleasant surprises in strong equity years and minor frustration with cap resets. Over a 20-year horizon, most crediting strategies have outperformed fixed alternatives, but past performance is not contractually guaranteed.

Variable Universal Life Insurance Policy (VUL)

A variable universal life insurance policy, also called a universal variable life insurance policy, invests cash value directly in sub-accounts. Cash value can grow substantially, but can also decline. Suitable only for investors with a long horizon, high risk tolerance, and strong financial discipline.

Universal Life Insurance Policy Pros and Cons

Advantages

- Lifelong coverage: A universal life insurance policy never expires, provided it remains adequately funded.

- Adaptability: Premium and death benefit flexibility make it uniquely suited to variable income self-employed individuals, commissioned professionals, and business owners. Consistently, they tell us it is the most useful feature they have.

- Tax-deferred growth: Cash value compounds without an annual tax drag. For high earners who have maxed out retirement accounts, this is meaningful.

- Living benefits: Policy loans and withdrawals provide access to capital without credit checks or market timing, a genuine liquidity advantage.

Disadvantages

- Complexity: Universal life insurance policies require regular policy reviews. A policy illustration is a projection, not a guarantee. When analyzing a policy’s health, we look for whether the cash value trajectory supports the death benefit through age 90 at a conservative interest assumption.

- Lapse risk: If underfunded, the policy lapses, terminating coverage and potentially triggering a taxable event on any gain inside the contract.

- Cost of insurance increases with age: Monthly deductions for the death benefit rise as you age, placing greater pressure on cash value in later years.

- Fees and charges: Administrative charges, premium load, and surrender charges (typically in the first 10–15 years) reduce net returns.

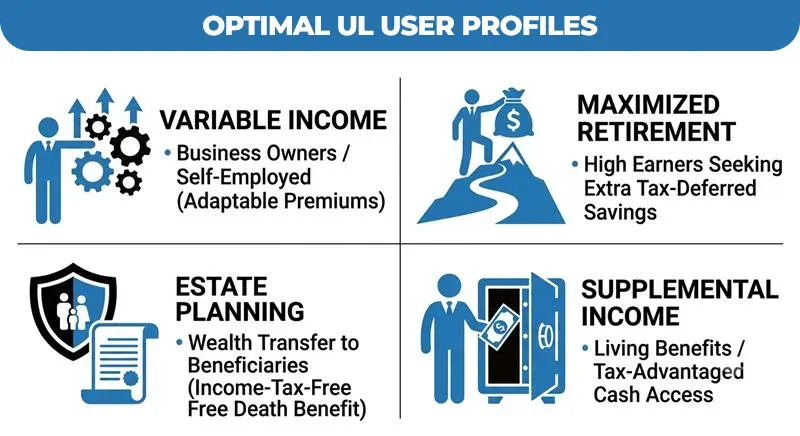

Why Would Someone Buy a Universal Life Insurance Policy?

Based on the profiles we encounter most frequently, universal life insurance is the strongest fit for:

- Business owners and the self-employed: Variable income makes fixed-premium whole life a poor fit. The ability to pay a large premium in a profitable year and a minimal premium in a slow year is a practical, business-friendly feature.

- High earners seeking additional tax-deferred growth: After maxing 401(k)s and IRAs, a properly structured IUL can function as an additional retirement savings vehicle with tax-advantaged income distribution.

- Estate planning scenarios: Individuals seeking to transfer wealth to the next generation benefit from the income-tax-free death benefit, particularly when policies are held inside an Irrevocable Life Insurance Trust (ILIT).

- Is universal life a good policy? For the right individual, yes, unambiguously. For someone who needs affordable temporary coverage with zero complexity, term life is the better recommendation. We never let a product drive the recommendation; the client’s situation drives the product.

Conclusion

Finalizing your financial strategy with a universal life insurance policy is a decisive act of stewardship that grants your family lasting protection while providing the dynamic flexibility needed to navigate life’s unpredictable economic shifts. By leveraging tax-deferred cash value growth and the ability to adjust premiums, you transform a traditional insurance product into a powerful financial tool.

Taking proactive control today ensures that your legacy remains secure and your coverage stays perfectly aligned with your changing lifestyle. We strongly encourage you to evaluate your long-term objectives and consult with a trusted advisor at Assurance Guru to stress-test your policy options—guaranteeing that your foresight delivers maximum value.

Frequently Asked Questions

What drawbacks does universal life insurance have?

The primary disadvantages include policy complexity, lapse risk if cash value is underfunded, rising insurance costs as you age, and fees that may reduce net returns over the policy’s long lifetime.

Is universal life a good policy?

It is an excellent choice for individuals who require permanent coverage, value financial flexibility, and commit to annual reviews. It is not suitable for those seeking simple, low-maintenance insurance solutions.

How does universal life insurance work?

You pay premiums, from which the insurer deducts monthly insurance costs and fees. Remaining funds are credited to your cash value account, keeping the death benefit active as long as needed.

Why would someone buy universal life insurance?

People choose this for its adaptability to variable income, permanent coverage, and estate planning goals. It also offers tax-deferred growth and potential access to funds during your retirement years.