Introduction

This is precisely the scenario that decreasing term life insurance was built to solve. It is a policy in which the death benefit reduces over time on a pre-set schedule, mirroring the way a long-term debt, most commonly a repayment mortgage, shrinks as it’s paid down.

As a strategic financial tool, its value lies in the efficiency it delivers protection exactly when your liability is largest, and then scales down in step with your risk, which keeps premiums significantly lower than other term products.

In our experience working with homeowners and small-business owners, decreasing term life insurance is one of the most misunderstood and most underused products in the personal finance toolkit. This guide walks through how the coverage works, who should consider it, how it compares to level term insurance, and how to size a policy to your actual debts.

How Does Decreasing Term Life Insurance Work?

Decreasing term life insurance is a form of term life insurance in which the death benefit, the amount paid to your beneficiary, declines at set intervals throughout the policy term, typically monthly or annually, according to a schedule fixed when the policy is issued.

Once the policy is in force, there’s little for the policyholder to manage. The insurer calculates the reduction schedule up front, and the coverage amount simply steps down in the background for the life of the policy.

The “Mirroring” Effect: A Mortgage Amortization Analogy

The clearest way to understand decreasing term life insurance is through amortization. On a standard repayment mortgage, each monthly payment reduces the outstanding loan balance, so the principal owed in year one is far higher than the principal owed in year twenty-five.

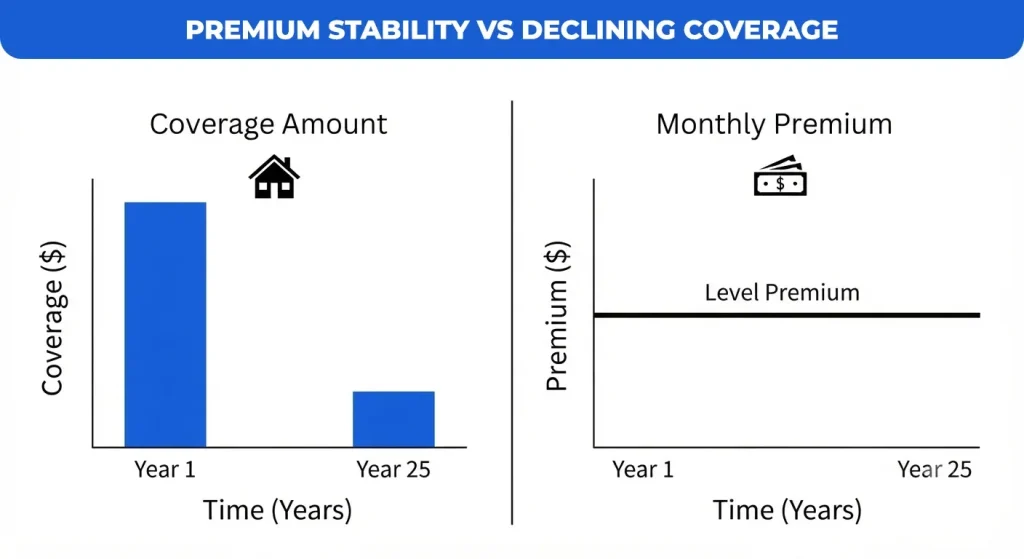

A decreasing term policy is engineered to track that same downward curve. Coverage is highest in the early years when your outstanding loan balance is largest and tapers as the loan is repaid, so the death benefit and the debt balance move in tandem.

Key Fact: Premiums Stay Level

This is the detail most buyers get wrong: although the coverage amount decreases, the monthly premium is fixed for the entire duration of the policy. The insurer front-loads the pricing based on the average risk across the full term, so your payment doesn’t fluctuate even as your payout shrinks.

| Pro-TipAsk your provider for the year-by-year coverage schedule, not just the starting face value. Two policies with an identical initial death benefit can decrease at very different rates. One may track a 3% mortgage amortization curve, another a steeper business-loan repayment curve. |

When to Choose Decreasing Term Life Insurance

Decreasing term life insurance is purpose-built for liabilities that shrink predictably over a fixed period. It is not designed to replace income indefinitely or to build wealth; it is protection-sized to a specific financial obligation.

Primary Use Cases

- Mortgage Protection: Often marketed as “mortgage life insurance,” this is the classic use case: the policy term matches the mortgage term, and the coverage curve is set to track the loan’s amortization schedule.

- Business Loans: Business partners frequently use decreasing term policies to protect a company or co-owners from a business loan or a stakeholder’s personal guarantee, ensuring the debt doesn’t fall on surviving partners.

- Personal/Student Loans: Large, fixed-term obligations such as a substantial personal loan or a co-signed student loan can be matched to a decreasing term policy so the balance doesn’t transfer to family members.

- Family Income Needs: Some households use a decreasing term policy to replace income during the child-rearing years, on the logic that the financial burden of raising children declines as they approach financial independence.

Key Consideration

Decreasing term life insurance is not a wealth-building tool. It carries no cash value, no investment component, and no savings feature; it exists purely to neutralize a specific, time-bound financial liability.

The Pros and Cons: Is It Right for You?

Pros

- Cost-Effectiveness: Because the insurer’s total risk exposure shrinks over the life of the policy, decreasing term life insurance is generally the cheapest form of term coverage for a given starting benefit amount.

- Budgeting: A level, predictable premium is simple to build into a household or business budget for the full policy term.

- Peace of Mind: The product is purpose-built to ensure a family can stay in the family home, or a business can absorb a partner’s debt, without a forced sale.

Cons

- Lack of Flexibility: The reduction schedule is fixed at issue. If you refinance, overpay your mortgage, or pay off a loan faster than planned, the policy won’t adjust to match your new balance.

- No Cash Value: Unlike whole or universal life insurance, there is no cash value component to borrow against or surrender for a payout.

- Expiration: Coverage ends at the end of the term. If you die after the policy expires, or after the death benefit has fallen close to zero, there is no meaningful payout left for costs like final expenses.

Decreasing Term vs. Level Term Life Insurance

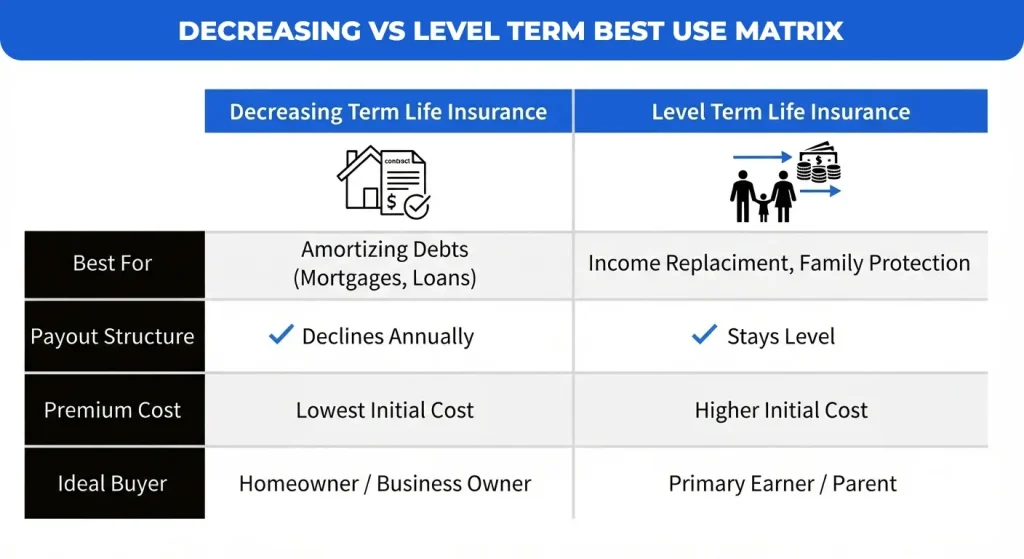

The decision between decreasing and level term life insurance comes down to what you’re protecting: a shrinking debt or a stable ongoing need.

| Feature | Decreasing Term Life Insurance | Level Term Life Insurance |

| Payout Structure | Declines on a fixed schedule (monthly or annually) | Stays constant for the entire term |

| Best For | A specific, amortizing debt (e.g., a repayment mortgage) | Long-term income replacement and general family protection |

| Premium Cost | Lowest of the term products | Higher than the decreasing term for the same initial face value |

| Cash Value | None | None |

| Ideal Buyer | Homeowner with a repayment mortgage or business loan | Primary earner supporting dependents or ongoing living expenses |

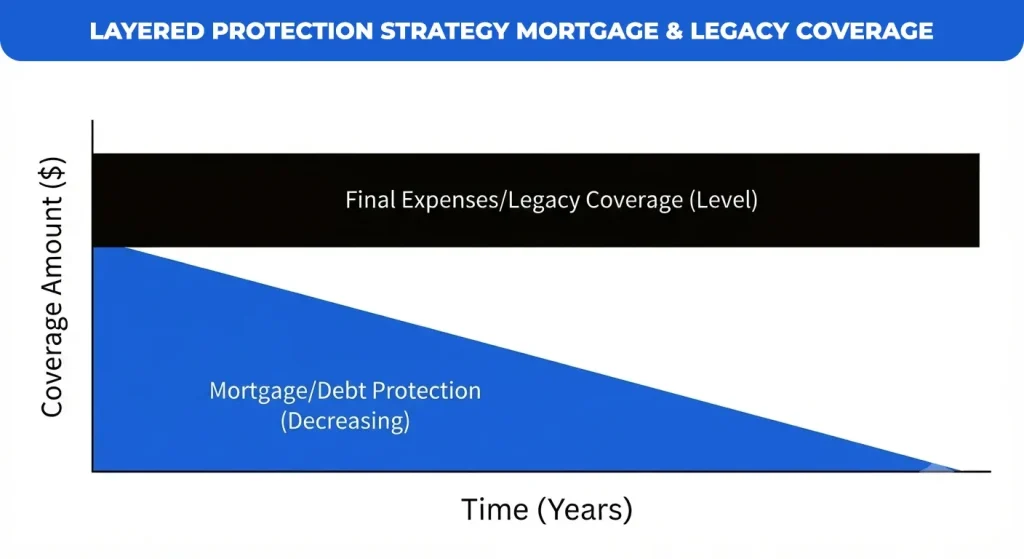

The “Mix and Match” Strategy

These two products aren’t mutually exclusive. A common structure pairs a decreasing term policy sized to the mortgage with a small, level-term policy earmarked for final expenses, estate costs, or a fixed legacy gift. This layered approach keeps overall premiums low while ensuring that at least some fixed benefit survives to the end of the term.

How to Determine Your Coverage Needs

Audit Your Debts

List every liability you want the policy to cover, along with its current balance, interest rate, and projected payoff date. This typically includes your mortgage, any business loans, and co-signed personal or student loans.

Match the Duration

Set the policy term to match the longest debt you intend to protect, commonly a 20-year or 30-year term aligned to a mortgage. A mismatched term is one of the most common structuring errors: a policy that expires before the mortgage does leaves a coverage gap in the final years.

Factor in Health and Lifestyle

Even though decreasing term life insurance is priced to be affordable, underwriters still weigh age, health status, and nicotine use when setting your premium. According to standard underwriting practice across the life insurance industry, applicants who apply earlier and in better health typically lock in materially lower rates, since risk is assessed at issue and then held at the same level for the full term.

Conclusion

Decreasing term life insurance serves as a surgical, purpose-built financial tool designed to neutralize specific, large-scale liabilities like amortizing mortgages or business loans. By aligning your coverage duration and payout schedule with your actual debt obligations, you ensure high-impact protection that remains significantly more cost-effective than standard level-term alternatives.

Ultimately, this strategy provides affordable peace of mind for homeowners and business owners seeking to prevent debt from burdening loved ones or partners. We recommend auditing your current amortization schedules and consulting a licensed advisor to confirm your policy structure precisely matches your long-term financial commitments, ensuring no coverage gaps remain.

Ready to Secure Your Home?

Don’t let your family’s future be defined by debt. Let the experts at Assurance Guru help you find a plan that perfectly matches your mortgage amortization schedule. Get Your Personalized Quote Today.