Introduction

Planning for the end of life is one of the hardest conversations a family can have. It sits at the intersection of grief, money, and mortality, three subjects most people would rather avoid. That avoidance has a cost. Without a plan in place, the burden of paying for a funeral often lands on a grieving spouse or adult child at the worst possible moment, forcing them to make expensive decisions under emotional pressure.

This is exactly why burial insurance for seniors exists. It is a small, affordable whole life policy built for one purpose: making sure the money for a funeral, cremation, or burial is there the moment it’s needed, without draining savings or forcing a family into debt. Securing a policy today is one of the most practical, loving gifts a senior can leave behind, not because it prevents grief.

This guide breaks down exactly how burial insurance works, what it costs at different ages, the policy types available, and the concrete steps to choosing coverage that fits both a budget and a health profile.

What Is Burial Insurance for Seniors?

Burial insurance, also called final expense insurance or funeral insurance, is a specialized, smaller-scale whole life insurance policy. It is conventional whole life insurance that has been scaled down and simplified, especially for end-of-life expenses; it is not a distinct product category created by marketers.

How It Differs from Term and Traditional Whole Life

- Term life insurance covers a set period, such as 10 or 20 years, and pays nothing if the insured outlives the term. It’s built for income replacement during working years, not for guaranteed final expenses.

- Traditional whole life insurance offers large death benefits, often $100,000 or more, and typically requires a full medical exam and years of underwriting history.

- Burial insurance sits in between: it’s permanent like whole life, but scaled down in coverage amount and underwriting complexity so seniors can qualify quickly.

Core Features

- Permanent coverage: the policy stays active for life as long as premiums are paid; there’s no expiration date to outlive.

- No medical exam for most policies: approval is typically based on a health questionnaire, not blood work or a physical.

- Modest coverage amounts: rather than replacing income, policies are often written between $5,000 and $40,000 and matched to reasonable burial and funeral expenses.

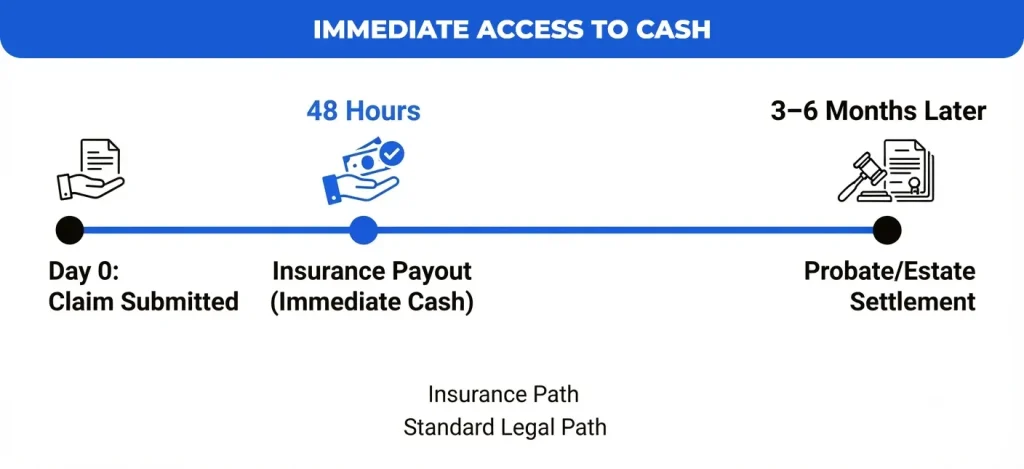

The real value isn’t the payout size, it’s the certainty. Burial insurance exists to make sure funeral homes and beneficiaries have immediate access to cash, often within 24 to 48 hours of a claim, instead of waiting for a probate process that can take months.

How Much Does Senior Burial Insurance Cost?

Premiums for burial insurance are underwritten on a handful of factors: age at purchase, gender, tobacco use, and current health history. Since there is typically no medical exam, insurers rely more on the information provided on the application; being truthful is important because a false statement could later endanger a claim.

Ballpark Monthly Estimates by Age

The table below reflects typical monthly premium ranges for a non-smoker in average health purchasing a $10,000 simplified-issue policy. Actual burial insurance quotes for seniors will vary by carrier, state, and underwriting class.

| Age Bracket | Female (approx.) | Male (approx.) | Notes |

| Age 60 | $28 – $40 / mo | $34 – $48 / mo | Widest carrier selection, lowest locked-in rate |

| Age 70 | $45 – $62 / mo | $55 – $75 / mo | Simplified issue is still widely available |

| Age 80 | $78 – $105 / mo | $95 – $130 / mo | Guaranteed issue becomes more common here |

| Age 85+ | $100 – $145 / mo | $120 – $170 / mo | Coverage caps are often lower; guaranteed issue standard |

These figures illustrate why timing matters. In comparison to a policy purchased at age 60 or 65, burial insurance for seniors over 80 and seniors over 85 costs significantly more per dollar of coverage.

| Key TakeawayOnce a policy is issued, the premium is locked in for life. The rate paid on day one is the rate paid at 95, even as health declines. Buying earlier isn’t just cheaper monthly; it caps that cost permanently. |

Understanding Policy Types: Which One Do You Need?

Nearly every burial insurance for seniors product falls into one of two underwriting categories. Choosing the right one prevents both overpaying and being under-protected.

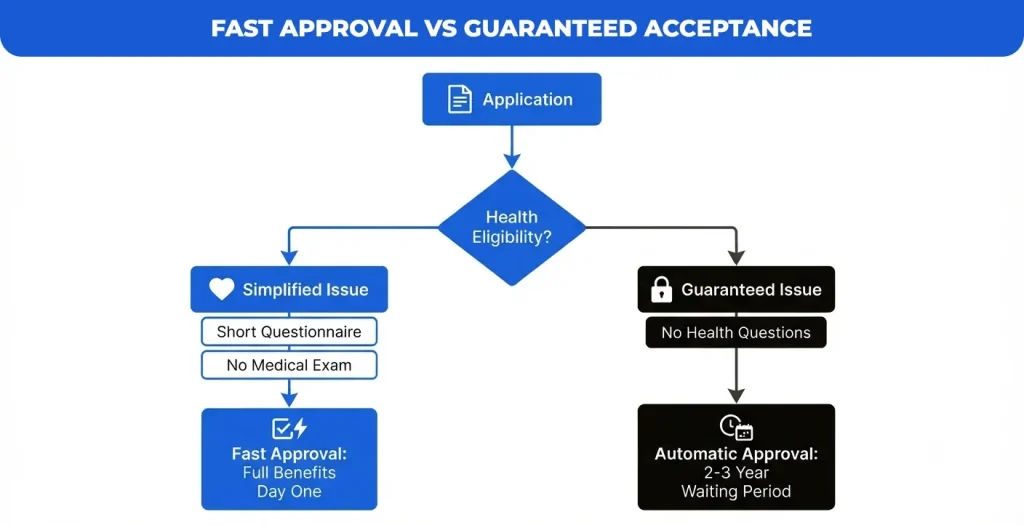

Simplified Issue

Simplified issue policies ask a short list of yes/no health questions, things like recent cancer diagnoses, heart conditions, or hospitalizations, but skip the medical exam and blood draw entirely. This is generally the best free burial insurance for seniors quote path for anyone in reasonably good health: approval is fast, often same-day, and full benefits apply from day one, including in the first two years.

Guaranteed Issue

There are no health-related questions in guaranteed issue policies. Approval is close to automatic for anyone within the eligible age range, which makes this the fallback for seniors with significant pre-existing conditions who don’t qualify for simplified issue. The tradeoff is a waiting period, typically two to three years, during which a death from natural causes pays out only a return of premiums.

Policy Type Comparison

| Feature | Simplified Issue | Guaranteed Issue |

| Health questions | Yes short questionnaire | None |

| Medical exam | No | No |

| Approval speed | Minutes to 1–2 days | Immediate to same-day |

| Waiting period | None gets the full benefit from day one | 2–3 years for natural causes |

| Best for | Seniors in average to good health | Seniors with major pre-existing conditions |

| Typical cost | Lower premium per $1,000 of coverage | Higher premium per $1,000 of coverage |

What Expenses Can Burial Insurance Cover?

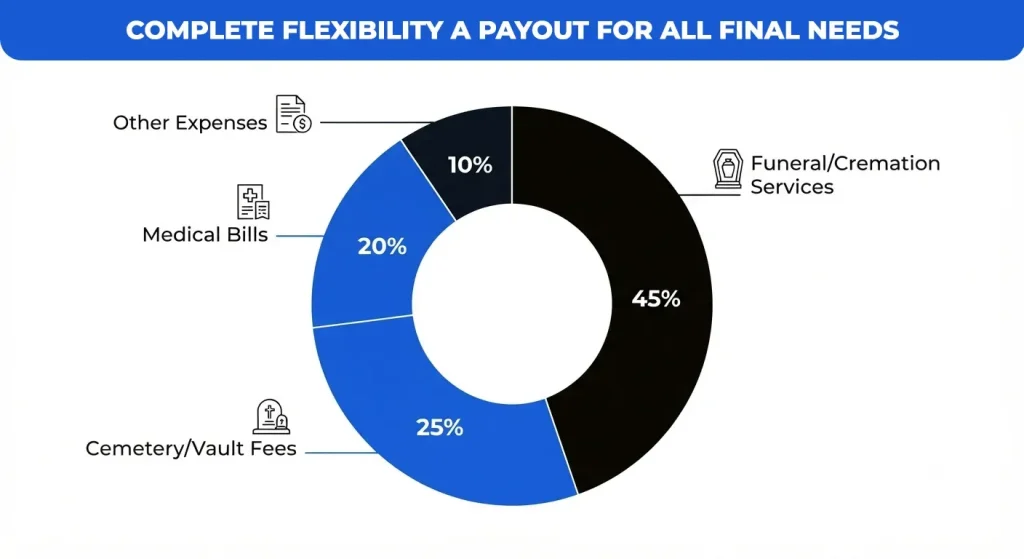

Because the policy pays a cash death benefit directly to a named beneficiary rather than to a funeral home, the money can be used however the family decides is most urgent. Common uses include:

- Funeral or cremation services, caskets, and urns

- Cemetery plot, headstone or grave marker, and vault or liner fees

- Outstanding medical bills or other small remaining debts

- Travel and lodging costs for out-of-town family members attending the service

This flexibility is often overlooked. Pre-need funeral contracts lock money into a single funeral home’s services; a burial insurance for seniors’ death benefit does not. If plans change, or if leftover funds exist after the service, the beneficiary keeps full control.

An Insider’s Perspective: What Families Actually Learn Too Late

After years of reviewing final expense claims and sitting in on family planning conversations, one pattern shows up more than any other: families don’t run out of money because the policy was too small; they run out of time. The single most common mistake isn’t underinsuring; it’s waiting. A senior who feels healthy at 68 often delays the decision by two or three years, and by the time they apply, a new diagnosis has pushed them out of simplified issue and into guaranteed issue.

families overestimate what a $15,000 policy actually buys. Local median costs matter more than national averages, and a policy sized off a national number can fall short by thousands. Calling local funeral homes directly, not searching for a national average online, consistently produces a more accurate coverage target.

According to the National Funeral Directors Association’s 2026 cost survey, the median cost of a funeral with viewing and burial in the United States now exceeds $8,300, before cemetery and vault fees are added, a figure that has climbed faster than general inflation over the past several years.

Conclusion

Securing burial insurance for seniors is an act of foresight that protects your loved ones from sudden financial burdens during a time of grief. By planning today, you transform unpredictable final expenses into a manageable monthly commitment, ensuring your legacy is handled with dignity and care.

Take the next step by evaluating local funeral costs and comparing quotes from multiple A-rated carriers to find the best value for your health profile. Whether you qualify for simplified issue or need guaranteed coverage, acting now secures a locked-in rate that provides lasting peace of mind for your family’s future.