Introducton

Thinking about life insurance for kids can feel strange, even a little morbid. Nobody wants to imagine the worst when they’re holding a newborn or watching a toddler take their first steps. That discomfort is normal, and it’s the main reason so many parents scroll past the topic entirely.

But the insurance industry doesn’t sell life insurance for my kids as an end-of-life product. It’s marketed as a long-term financial tool, a way to lock in low rates while a child is young and healthy, and to guarantee they can get coverage later, even if their health changes. That pitch is worth examining closely, because it’s only partly true.

This guide breaks down how a life insurance policy for kids actually works, what it costs, where it shines, and where it falls short compared to alternatives like 529 plans and custodial brokerage accounts. No sales script, just the mechanics, so you can decide for yourself whether it belongs in your family’s financial plan.

What Is Life Insurance for Kids and How Does It Work?

Children’s life insurance is almost always sold as whole life insurance for kids, permanent coverage that lasts the child’s entire life, rather than a temporary term policy. Some parents add coverage through a rider on their own adult policy instead, which works a little differently and is covered in the next section.

Every standalone policy has two moving parts:

- The death benefit is the payout if the child dies during the coverage period. This is the part everyone hopes never gets used.

- The cash value component a tax-deferred savings bucket that grows slowly over decades and can eventually be borrowed against or withdrawn.

The parent or grandparent owns the policy and pays the premiums until the child reaches the age of majority, 18 in most states, 21 in a few. At that point, ownership transfers to the now-adult child, who can keep the policy, cash it out, or add more coverage.

One thing that surprises a lot of parents: coverage caps for minors are much lower than adult policies. According to standard industry underwriting practices, most insurers cap life insurance for kids under 18 somewhere between $50,000 and $75,000, regardless of how much the parents are willing to pay in premiums.

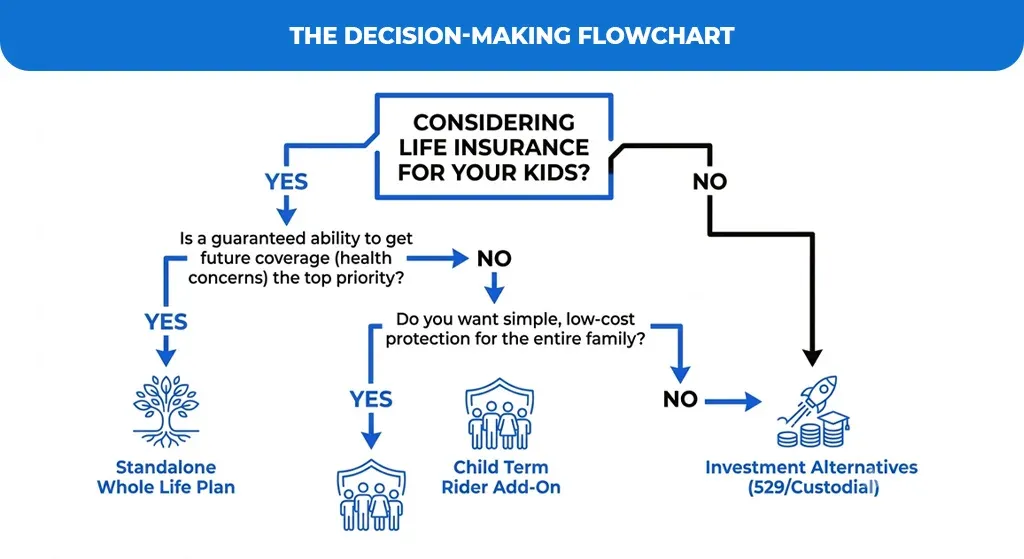

The Two Ways to Insure a Child

There are really only two paths here, and they behave very differently.

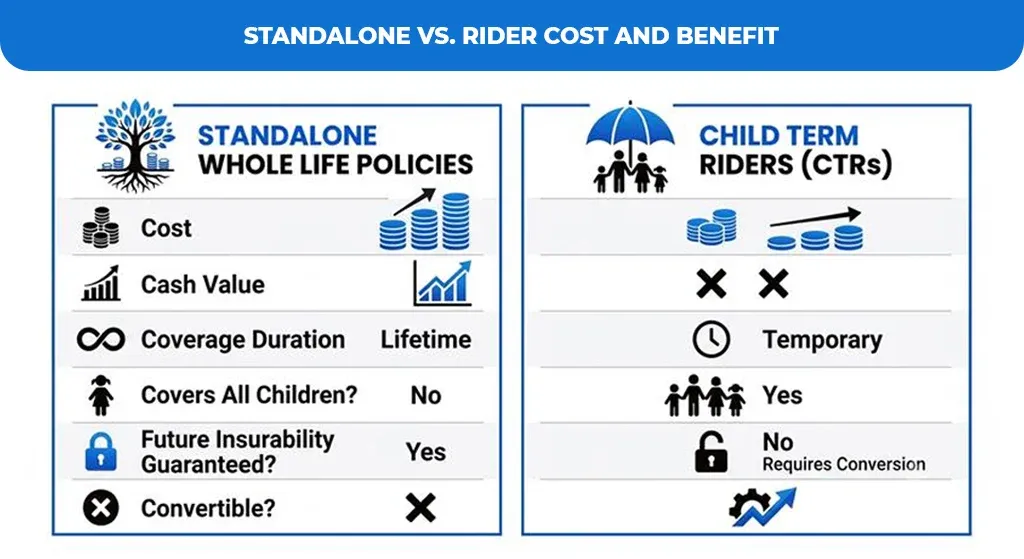

Standalone Whole Life Policies

A standalone whole life insurance policy is its own contract, independent of anything the parents carry. It builds cash value over time, and the premium is fixed for life. The amount you pay at age one is the same amount you’d pay at age fifty, assuming the policy stays in force.

Child Term Riders (CTRs)

A child term rider is an add-on to a parent’s existing term or whole life policy, rather than a separate contract. A few features set it apart:

- One flat rider fee typically covers every child in the household, not just one.

- It’s dramatically cheaper than a standalone policy, often described as costing pennies a day.

- Coverage expires when the child hits a certain age, usually somewhere between 21 and 25.

- Most riders include a guaranteed conversion option, letting the child switch to an adult permanent policy later with no medical exam.

| Feature | Standalone Whole Life | Child Term Rider (CTR) |

| Cost | Regular monthly premium per child | Single flat fee, covers all kids |

| Cash value | Yes, builds slowly over decades | No |

| Duration | Lifetime | Expires at 21–25, convertible |

| Best for | Parents wanting permanent coverage + savings | Parents wanting cheap, simple protection |

The Pros of Life Insurance for Kids

Supporters of child life insurance point to a handful of genuine advantages.

Guaranteed future insurability is the biggest one. If a child develops a chronic condition, juvenile diabetes, a genetic predisposition that shows up on family screening, or another health issue, a policy locked in during infancy protects their ability to get coverage later, even if an adult insurer would otherwise decline or upcharge them heavily.

Locked-in, rock-bottom rates come next. Premiums are priced on age and health at the time of purchase, so insuring a healthy infant is about as cheap as this product ever gets, and that rate stays static for life.

A small cash value nest egg builds in the background. It’s not going to fund a full college tuition on its own, but the child can eventually tap it for education costs, a down payment, or vocational training.

Final expense protection rounds it out. If the unthinkable happens, the death benefit can cover funeral costs and give grieving parents room to step back from work without an added financial crisis on top of everything else.

The Cons and Criticisms of Child Insurance

Most independent financial planners are considerably more skeptical, and the criticisms are worth taking seriously.

Low rate of return is the headline problem. The cash value component grows so slowly that it can take 10 to 20 years just for the accumulated value to catch up to the premiums already paid. Early payments go mostly toward fees and administrative costs, not savings.

Opportunity cost is the second issue. The same monthly premium, redirected into a 529 plan, a UTMA/UGMA custodial account, or a plain index fund, would very likely produce a far larger balance by the time the child is an adult.

Inflation quietly erodes the payout. A $25,000 death benefit locked in today buys a lot less in 40 or 50 years. What looks like meaningful coverage now may look almost symbolic by the time it would ever be paid out.

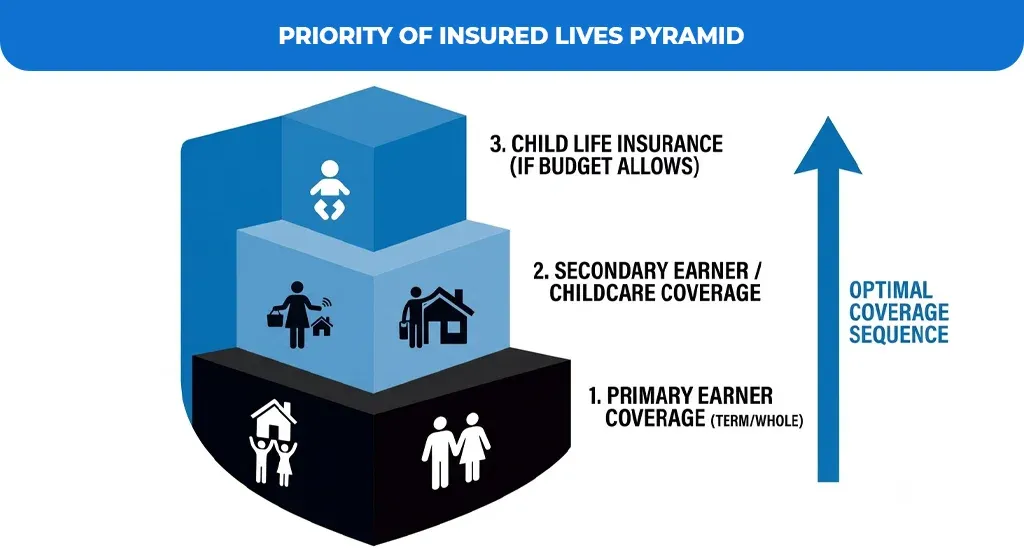

Misplaced priorities is the argument that stings the most, but it’s hard to dispute: life insurance exists to replace lost income, and children don’t earn income. Most advisors agree that the priority should always be maximizing the parents’ own coverage first, before the people whose death would actually create a financial gap.

Best Life Insurance for Kids: Market Leaders

A handful of names dominate search results and actual policy sales.

Gerber Life Grow-Up Plan is the most recognized standalone product on the market. It’s built specifically as cheap life insurance for kids, with eligibility starting at 14 days old and running through age 17, and coverage that automatically doubles at 18 with no added premium. Entry-level plans start under $4 a month for $5,000 in coverage.

Globe Life insurance for kids and Mutual of Omaha are two common direct-to-consumer alternatives. Both skip the medical exam and lean on fast, simplified online underwriting, which appeals to parents who want something set up in a single sitting.

| Provider | Entry Coverage | Approx. Monthly Rate (Infant) | Medical Exam |

| Gerber Life Grow-Up® | $5,000 | ~$3.70/month | Not required |

| Globe Life | Varies by state | Low, simplified pricing | Not required |

| Mutual of Omaha | Varies by state | Low, simplified pricing | Not required |

Rates above reflect general 2026 baseline pricing for healthy infants under age one; actual premiums vary by state, including for parents researching life insurance for kids in South Carolina and other states with their own regulatory pricing rules.

What to Consider Instead of a Child Life Insurance Policy

Before signing up for the best whole life insurance for kids a search engine can find, it’s worth stacking it up against three alternatives that usually deliver more financial firepower.

- 529 Education Savings Plans: Contributions grow tax-free, and withdrawals for qualifying education costs are tax-free too. Recent rule changes even allow unused funds to roll into a Roth IRA for the child, which removes a lot of the old “what if they don’t go to college” hesitation.

- Custodial Brokerage Accounts (UTMA/UGMA): These give a child unrestricted market exposure, without the drag of insurance fees eating into early returns. There’s more flexibility, but also less structure. The money isn’t earmarked for anything specific.

- Boosting the parents’ own life insurance: A larger term policy on the primary earner protects the family’s actual lifestyle and future needs far more meaningfully than a small policy on a child who isn’t generating income yet.

Conclusion

Deciding whether life insurance for kids is a wise financial safeguard or an unnecessary expense ultimately depends on your family’s specific health history and long-term goals. While permanent policies offer the undeniable peace of mind of locking in guaranteed future insurability at rock-bottom rates, the slow growth of their cash value rarely matches the wealth-building power of dedicated equity investments.

For most parents, the smartest financial blueprint means prioritizing your own adult coverage first, adding a budget-friendly child term rider, and funneling any extra savings into high-yield vehicles like 529 plans. This balanced approach protects your household today without sacrificing your child’s future financial growth.

Ready to find the perfect safety net for your family?

Don’t navigate the complex world of insurance alone. Whether you decide on a budget-friendly child term rider or want to maximize your own coverage, let our experts do the heavy lifting. Head over to Assurance Gurus right now to compare personalized quotes and lock in the absolute lowest rates for your peace of mind.