Introduction

A cash value life insurance policy is a type of permanent life insurance, including whole, universal, and variable life, that combines a tax-free death benefit with a built-in savings component called cash value. A portion of every premium payment goes toward the cost of insurance, while the remainder accumulates inside the policy on a tax-deferred basis. Unlike term life insurance, which has no cash value and expires after a set period, a cash value life insurance policy lasts your entire life as long as premiums are paid, and the accumulated cash can be borrowed against or withdrawn to help fund tuition, emergencies, or retirement income.

In our experience working with clients across every life stage, the appeal of a cash value life insurance policy isn’t just the death benefit; it’s the flexibility of having a living benefit you can tap into decades before that benefit is ever paid out. This guide breaks down how cash value grows, how to access it safely, who it’s actually built for, and the risks that too many policyholders learn about the hard way.

What You’ll Learn in This Guide

- How the cash value component grows inside a permanent policy

- The safest ways to access your funds without triggering taxes or lapsing your coverage

- Who genuinely benefits from a cash value life insurance policy, and who doesn’t

- The hidden costs, risks, and “premium trap” that catch policyholders off guard

- How to monitor and maintain your policy so it performs as projected

What Is a Cash Value Life Insurance Policy?

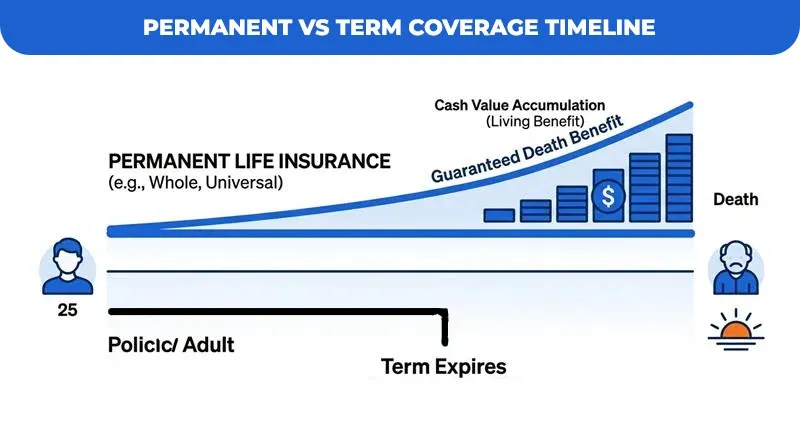

A cash value life insurance policy is a subset of permanent life insurance, meaning Whole Life, Universal Life, or Variable Life that features a savings or investment component layered on top of the standard death benefit. This distinguishes it sharply from term life insurance, which provides pure protection for a fixed number of years (typically 10, 20, or 30) and builds no cash value whatsoever.

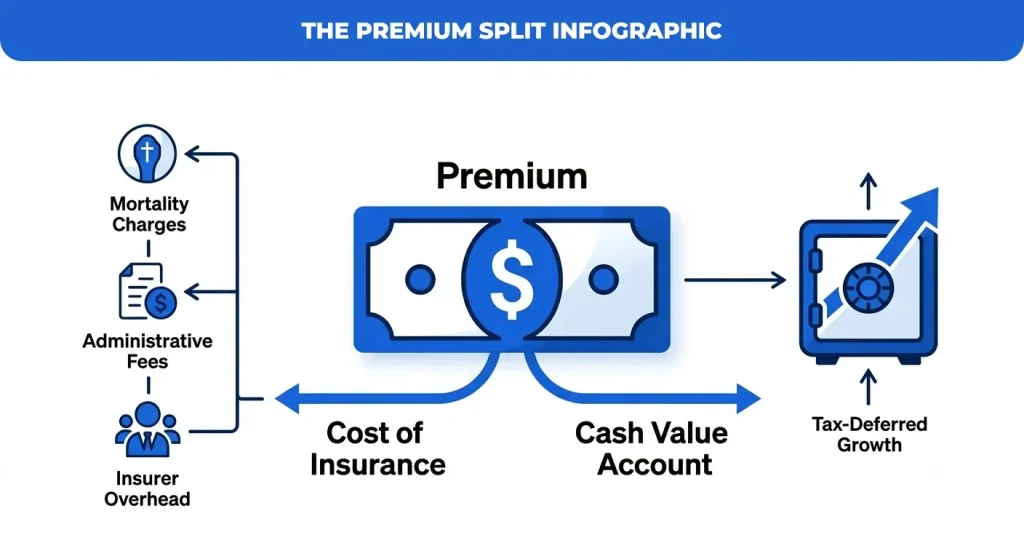

The “Two-in-One” Value Proposition

Every premium dollar you pay into a cash value life insurance policy is split. A portion covers the cost of insurance (mortality charges, administrative fees, and the insurer’s overhead), while the remainder is funneled into a separate cash account that earns interest or market-linked returns, depending on the policy type. Over time, this account becomes an asset you can access while you’re still alive, something a term policy can never offer.

Lifelong Coverage, Not Temporary Protection

Unlike term life insurance, a cash value life insurance policy covers you for your entire life, provided premiums are paid as scheduled. This is the core reason these policies cost more upfront: you’re not just buying a temporary safety net, you’re funding a permanent asset that’s guaranteed to pay out eventually, rather than betting on whether you’ll pass away within a specific term window.

How Does Cash Value Accumulation Work?

Cash value accumulation functions as a form of forced savings built directly into your insurance premium. Because contributions happen automatically with every payment, policyholders build savings discipline without needing to actively manage a separate account. Growth inside the cash value of a life insurance policy is tax-deferred, meaning you don’t owe taxes on gains as they accumulate year over year, only under specific circumstances when funds are withdrawn improperly.

Growth Factors by Policy Type

| Policy Type | Growth Mechanism | Risk Level |

| Whole Life | Guaranteed, stable growth set by the insurer | Low, predictable, but conservative |

| Universal Life | Flexible, often tied to a market index with a floor | Moderate flexible premiums, variable returns |

| Variable Life | Invested directly in sub-accounts (stocks/bonds) | High upside, real downside exposure |

Why Early-Year Growth Feels Slow

A common challenge we see is new policyholders expecting rapid cash value growth in years one through three, only to find balances climb slowly at first. This is by design: administrative costs and the insurance cost load, including agent commissions, are weighted toward the early years of the policy. Most cash value life insurance policies don’t show meaningful net accumulation until year five or later, which is why these policies are unsuitable for anyone who may need the funds in the short term.

Key Benefits: Why Consider a Cash Value Policy?

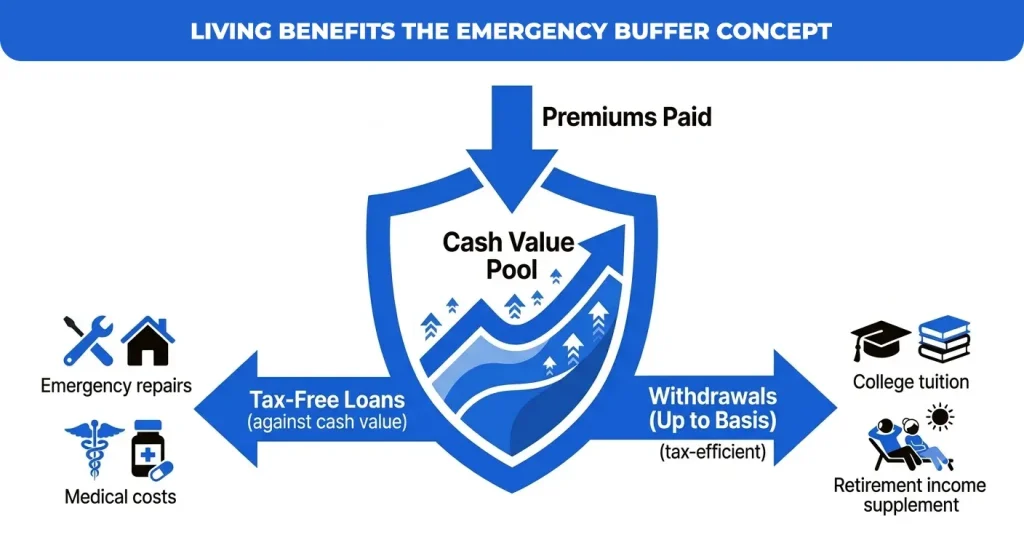

Financial Flexibility

One of the most practical advantages of a life insurance policy with cash value is the ability to borrow against the policy or make withdrawals for major expenses, such as college tuition, a down payment, an emergency fund, or supplemental retirement income. Policy loans typically don’t require credit checks or a formal approval process, since you’re effectively borrowing against your own asset.

Tax Advantages

Death benefits from a cash value life insurance policy are generally paid to beneficiaries income-tax-free. In addition, loans and withdrawals up to your cost basis (the total premiums you’ve paid in) are typically not taxed, making the policy a useful tax-advantaged tool when structured properly.

Estate Planning Value

Because death benefit proceeds typically bypass probate, a cash value life insurance policy can provide heirs with immediate liquidity to cover estate taxes, debts, or final expenses without waiting on the often lengthy probate process.

When to Consider a Cash Value Policy

- You need lifelong coverage rather than coverage for a defined period

- You’ve already maxed out other tax-advantaged accounts, such as a 401(k) or IRA

- You want a conservative “buffer” asset that complements a more aggressive investment portfolio

Risks and Important Considerations

Higher Costs

Premiums for a cash value life insurance policy are significantly higher than term life premiums for the same death benefit, since you’re funding both protection and a savings component simultaneously.

Impact on the Death Benefit

Any outstanding policy loans or withdrawals reduce the final payout to beneficiaries. If a loan balance grows large enough with accrued interest, it can substantially erode or, in worst cases, eliminate the intended death benefit.

The “Premium Trap” and Risk of Lapse

If the cash value drops too low to cover internal policy charges and premiums aren’t kept current, the policy can lapse. A lapse with an outstanding loan can also trigger a significant, unexpected tax bill, since the IRS treats the forgiven loan amount above cost basis as taxable income. In our experience, this is the single most damaging surprise we see policyholders encounter, and it’s entirely avoidable with proper monitoring.

Surrender Charges

Exiting a cash value life insurance policy in its early years, typically within the first 10 to 15 years, can trigger steep surrender charges that significantly reduce the amount you actually receive.

Strategies for Success: Monitoring Your Policy

The “Set It and Forget It” Myth

It’s a common misconception that permanent insurance is a buy-and-hold option. Interest rate changes, market volatility, and shifts in the cost of insurance can all cause actual policy performance to diverge from original projections. Periodic reviews are essential to catching underperformance before it becomes a lapse risk.

Working with a Broker

We recommend annual or, at a minimum, biennial check-ins with a licensed broker or advisor to re-evaluate your coverage needs against major life changes, such as marriage, a new mortgage, the birth of a child, or business growth, and to confirm the policy is still tracking toward its original illustration.

Actionable Tip: Track Your Cost Basis

Keep detailed records of your cost basis (total premiums paid) throughout the life of the policy. This single number determines the tax treatment of any future withdrawal, and policyholders who lose track of it often overpay in taxes or misjudge how much they can safely access.

Conclusion

A cash value life insurance policy is a long-term financial commitment, not a quick savings vehicle. It rewards patience, consistent premium payments, and periodic oversight, and in exchange offers lifelong protection paired with a tax-advantaged living benefit few other financial products can replicate.

Before moving forward, compare your financial goals, pure protection versus long-term liquidity and flexibility, and talk through your specific situation with a licensed financial advisor or insurance professional to determine whether a cash value life insurance policy fits your unique portfolio.

Is a Cash Value Policy Right for Your Financial Portfolio?

Determining whether a cash value policy aligns with your broader financial goals requires an analysis of your tax bracket, liquidity needs, and long-term objectives. At Assurance Guru, our advisors help you determine if this tool is a smart addition to your wealth strategy.